2026 is shaping up as another tough year for layoffs and hiring freezes, but it is more a continuation and restructuring phase than a completely new “mass bloodbath” like early 2023.

What is actually happening in 2025–2026

Tech layoffs re-accelerated through 2025, with over 100,000 tech workers cut and more than 200 tech companies reducing headcount globally.[economictimes]

Many of these 2025 cuts came from large players (Amazon, Intel, TCS, Google, Meta) shifting priorities, especially towards AI and away from older or lower‑margin lines.[tomshardware]

Early 2026 has already seen fresh rounds from firms like Meta (Reality Labs), Citigroup, and BlackRock, suggesting the 2025 pattern is carrying into this year.[business-standard]

Why leaders expect more cuts in 2026

Surveys of executives show a clear bias towards staying lean: roughly two‑thirds of CEOs say they plan to either cut or hold headcount flat in 2026 rather than grow it.[saastr]

One 2025 survey of 1,000 US business leaders found half had already pulled back on hiring, nearly 40% had done layoffs in 2025, and a majority expected further layoffs to be likely in 2026.[hrdive]

Another survey of hiring managers reported that more than half expect layoffs in 2026 and see AI as a top driver of those cuts, especially for white‑collar roles.[informationweek]

AI, “invisible unemployment,” and who is most exposed

A growing chunk of the pain is “invisible”: roles quietly eliminated via attrition, aggressive performance management, relocation/RTO pressure, and not backfilling departures, so the headline layoff numbers understate the chill.[saastr]

Economists and industry observers describe 2026 as a “Great Freeze”: fewer new openings, more restructuring, and companies using AI plus process changes to do the same work with fewer people.[linkedin]

High‑salary staff without strong AI or automation skills, recently hired employees, and some entry‑level roles are viewed by executives as the highest‑risk groups for future cuts.[hrdive]

How this likely feels in tech and AI infra

For people in tech, 2026 is likely to feel like a grinding reset: fewer net new roles, more churn between companies, and continued pressure on anything tied purely to speculative AI or overbuilt infra.[info.siteselectiongroup]

At the same time, companies are heavily investing in a smaller core of people who can build, operate, and productize AI and automation, including infra and observability talent, rather than cutting across the board.[finalroundai]

Practical implications for you

Treat 2026 as a year to be defensive:

Make sure your current role is visibly tied to cost savings, reliability, or revenue, not just “innovation theatre”.[perplexity]

Double down on AI‑adjacent skills (MLOps, GPU/AI infra, automation with AI copilots) so you’re in the “kept and retrained” cohort rather than the expendable one.[tomshardware]

If you’re in AI/data‑center/infra, the risk is more about over‑concentration in a fragile employer or product line than the whole category disappearing; diversified or sovereign‑backed infra tends to ride out the cycle better.[perplexity]

In 2025, economic analysts and sociologists, most notably in a widely discussed analysis by The Economist, have identified Generation X (born 1965–1980) as the “real loser generation” due to a unique convergence of financial and social setbacks.

The primary reasons Gen X is characterized this way include:

Wealth Lag: Despite being at their peak earning years, Gen X has significantly less wealth than previous generations at the same age. For example, 2025 data shows that Millennials at age 31 have roughly double the wealth that the average Gen Xer had at that same point in their life.

The “Sandwich” Squeeze: Gen X is currently under intense pressure as the “Sandwich Generation,” simultaneously caring for aging parents and supporting their own children. Over 54% of Americans in their 40s are now balancing these dual caregiving roles.

Poor Market Timing: This cohort faced a “lost decade” in the stock market during the 2000s, precisely when they should have been building wealth. They entered the workforce during recessions and were hit by the 2008 financial crisis just as they were entering their prime career stages.

Invisible at Work: Many Gen Xers report feeling invisible in a corporate landscape that increasingly values younger “tech-native” talent (Millennials/Gen Z) or retains aging Baby Boomer leaders. Some corporations are reportedly “skipping over” Gen X for C-suite promotions in favor of younger leaders.

Retirement Anxiety: Unlike Boomers who often had stable pensions, Gen X must rely on volatile 401(k) plans and a shaky Social Security outlook. Nearly 60% of Gen Xers now expect to work past age 65.

Cultural Neglect: Often called the “latchkey kids” or the “forgotten generation,” Gen X is largely ignored in the cultural “generational wars” between Boomers and Millennials. They lack the media attention and political influence of the larger cohorts that flank them.

We have some wins

Gen X has been pivotal in education, technology, leadership, and cultural change, often acting as the **bridge** between older and younger cohorts.

Tech and innovation advantages

– Gen X was the first cohort to grow up alongside personal computers, the internet, and mobile phones, giving them a rare comfort with both analog and digital worlds.

– Many Gen X entrepreneurs lead in adopting new technologies and using them to create innovative business models, especially in tech, finance, and e‑commerce.

Educational and career gains

– Gen X was the first generation to face a labor market that effectively required postsecondary education for good jobs and responded with higher college attainment than Baby Boomers at similar ages.

– College‑educated Gen Xers typically enjoy higher incomes and greater wealth than less‑educated peers, showing that many in this cohort successfully leveraged education into upward mobility.

Leadership and workplace strengths

– Gen X workers are now heavily represented in senior and executive roles, bringing deep institutional knowledge, strong work ethic, and problem‑solving skills to leadership.

– Employers see Gen X as especially adaptable and resilient, having navigated repeated economic and technological shifts while still driving transformation in their organizations.

Bridge between generations

– Positioned between Boomers and Millennials, Gen X is widely described as a mediator generation that understands traditional hierarchies and newer, more fluid work cultures, smoothing communication across age groups.

– In workplaces, Gen X frequently acts as the connector between colleagues who struggle with digital tools and those who are “always online,” helping teams stay cohesive and productive.

Cultural and lifestyle benefits

– Gen X helped define late‑20th‑century and early‑internet culture: from alternative music and independent film to early online communities and gaming, leaving a lasting cultural footprint.

– Compared with older cohorts, many Gen Xers place a high value on work‑life balance and flexibility and have been key drivers in normalizing remote work, flexible hours, and more autonomous, less hierarchical work styles.

Conclusion

Yep, balancing things up, I can conclude we are the losers…

AI refers to machines performing tasks that typically require human intelligence. AGI is AI with general, human‑level cognitive abilities across a wide range of tasks. ASI is a hypothetical AI that surpasses human intelligence in virtually all domains.

Overview

AI or ANI (Artificial Narrow Intelligence): specialized AI that excels at specific tasks (e.g., image recognition, playing chess, language translation). It’s the most common form in use today.

AGI (Artificial General Intelligence): systems with broad, human‑level capabilities—understanding, learning, reasoning, and applying knowledge across many domains.

ASI (Artificial Superintelligence): a level of intelligence that greatly exceeds human capabilities in all areas.

Scope of tasks

ANI: narrow scope, task-specific

AGI: wide, adaptable reasoning across domains

ASI: superior performance in everything, including creativity and problem‑solving

Learning and adaptability:

ANI: learns within fixed parameters and datasets

AGI: can learn from diverse experiences and transfer knowledge

ASI: continuously self‑improves beyond human constraints

Current state and timelines

ANI is ubiquitous today, powering search, assistants, recommendations, and more.

AGI remains aspirational; estimates vary widely among researchers, with no consensus on when or even if it will be achieved.

ASI is speculative science fiction at present; most experts agree it would require breakthroughs beyond AGI.

Potential implications

Economic and labor impacts: automation of complex tasks could shift job roles and demand new skills.

Safety and governance: AGI/ASI would raise significant ethical, safety, and governance questions, including alignment with human values.

Research and science: AGI could accelerate discovery across fields, from medicine to physics.

Common misconceptions

AGI does not imply immediate, conscious machines with emotions; it implies broad cognitive capabilities.

ASI does not mean instant, uncontrollable intelligent beings; it depends on many speculative breakthroughs and safety frameworks.

Summary

ANI: specialized AI for specific tasks

AGI: human‑level general intelligence across tasks

ASI: intelligence far surpassing human capabilities

How do AGI and ASI differ in capabilities

AGI is defined as AI that can match human-level intelligence across many domains, while ASI is a hypothetical future AI that would far surpass the best human minds in virtually all areas of cognition. Both are more capable than today’s narrow AI, but ASI adds superhuman scale, speed, and depth along with the ability to improve itself far beyond human limits.softbank+3

Core capability difference

AGI: Human-level performance on most intellectual tasks, including learning, reasoning, planning, and adapting across domains, similar to a broadly educated person.wikipedia+1

ASI: Superhuman performance in essentially every intellectual task, including science, strategy, creativity, and long-term planning, not just faster computation.moontechnolabs+2

In short, AGI aims to do what humans can do; ASI aims to do far more than humans can do, in both breadth and depth.netguru+1

Learning and self‑improvement

AGI: Can learn from diverse data and experiences, transfer knowledge between domains, and adapt to new tasks, but its self‑improvement is still constrained by design and human oversight.softbank+2

ASI: Typically defined as recursively self‑improving—able to redesign its own algorithms, generate its own training data, and continually increase its capabilities without direct human guidance.creolestudios+2

This recursive self‑improvement is a key reason ASI is often linked to the “intelligence explosion” or technological singularity.netguru+1

Scope and problem‑solving

AGI: Expected to handle any task a human knowledge worker could, from scientific research to teaching, software engineering, or policy analysis, with strong but roughly human‑comparable judgment.kanerika+2

ASI: Would solve problems beyond human comprehension, discover patterns humans cannot see, and generate new scientific theories or technologies at a pace and sophistication that humans could not match.moontechnolabs+2

Where AGI might collaborate with humans as a peer, ASI would function more like an extremely powerful, alien-level expert.

Table: AGI vs ASI capabilities

Aspect

AGI (General)

ASI (Superintelligence)

Intelligence level

Roughly human-level across many domains.wikipedia+2

Vastly beyond the best human experts in all domains.softbank+2

Learning style

Learns and generalizes across tasks like a human.softbank+2

Creates its own learning strategies and data; recursively self‑improving.softbank+1

Problem‑solving

Solves most tasks humans can, with high flexibility.moontechnolabs+1

Cracks problems humans cannot even fully specify or understand.softbank+2

Speed and scale

Similar cognitive range to humans, but faster on some tasks.moontechnolabs

Operates at machine speed on global, massive‑scale data streams.moontechnolabs+1

Novel discovery

Can assist and sometimes lead human‑level research.moontechnolabs+1

Drives radical breakthroughs in science, technology, and strategy autonomously.moontechnolabs+1

Self‑modification

Limited or controlled self‑improvement.softbank+1

Open‑ended self‑modification and optimization of its own code and goals (in many visions).softbank+2

Status today

AGI: Still not achieved; current systems are closer to advanced narrow or “weak” forms of generality, and AGI remains an aspirational research target.viso+2

ASI: Entirely speculative at present, dependent on first reaching robust AGI and then enabling powerful recursive self‑improvement.kanerika+2

If you want to go deeper, the next useful dimension is risk and governance differences: why AGI raises big alignment questions, and why ASI raises civilization‑level control questions.

What are real world uses of AGI today

There are no widely accepted, deployed AGI systems in the strict “human‑level general intelligence” sense today; what exists are advanced narrow or “proto‑AGI” models being used in many real‑world applications. Most concrete use cases branded as “AGI” are actually powerful generative or multimodal AI applied across multiple tasks rather than true general intelligence.sidetool+3

Important clarification

No consensus that AGI exists yet: Surveys and 2025 overviews still describe AGI as a future milestone that requires breakthroughs in general problem‑solving and knowledge transfer.kanerika+1

Marketing vs reality: Many articles and vendors use “AGI” aspirationally for advanced models, but technical write‑ups usually treat them as steps toward AGI, not fully general minds.techrevolt+2

So “real‑world uses of AGI” today are better described as uses of advanced AI that show some generality but remain below true AGI.

Advanced AI uses often framed as AGI‑like

Autonomous task agents in business: End‑to‑end agents can plan, call tools, and complete tasks such as drafting contracts, generating code, and running simple workflows with minimal oversight.cloud.google+1

Cross‑domain copilots: Enterprise copilots (e.g., Google’s Gemini‑based Workspace assistants) summarize mail, generate documents, analyze sheets, and answer questions over internal knowledge, acting as a general knowledge worker assistant within one organization.cloud.google

These systems show broader versatility than classic narrow AI but still lack robust, human‑level general understanding and autonomy.scientificamerican+1

Examples often cited as “AGI use cases”

Healthcare decision support: Systems like IBM’s Watson Health analyze patient records and large medical literature corpora to suggest treatment options and support oncology decisions, sometimes cited as early AGI‑style reasoning in a specialized domain.ibm+1

Industrial optimization and predictive maintenance: Large AI systems monitor sensor data, detect anomalies, and optimize complex production lines or logistics networks, adjusting schedules and predicting failures in near real time.ibm+1

These fit “powerful domain‑general within a vertical” more than “fully general intelligence.”

Multimodal “proto‑AGI” applications

Customer service and sales: Multimodal models that understand text, voice, and sometimes images are used for richer customer support, sentiment‑aware responses, and context‑aware recommendations.weforum+2

Knowledge and research assistance: Large models are used for legal analysis, financial modeling aid, and code generation, giving human experts faster access to cross‑domain information and draft reasoning.sidetool+1

Some commentators argue these systems are “chasing and occasionally catching” AGI capabilities in narrow slices, but they are not yet considered true AGI by most researchers.techrevolt+2

How to interpret “AGI in the real world” today

In research and journalism, “AGI use cases” usually mean: “Here’s what AGI would do in healthcare, manufacturing, logistics, etc.” rather than deployments of a confirmed AGI.kanerika+1

In industry and marketing, the term often labels very capable general‑purpose assistants or agents built on frontier generative models that are still narrow compared with human general intelligence.sidetool+2

If you want, the next step can be mapping specific “AGI‑like” patterns (tool‑using agents, long‑horizon planners, cross‑modal perception) to concrete systems you’re likely to encounter in enterprise or developer workflows.

What is the progress to ASI – how near are we?

Artificial superintelligence (ASI) does not exist today, and expert views on when or whether it will emerge vary enormously, from “possibly this century” to “not with current approaches, if ever.” The only honest summary is that progress is rapid toward stronger AI systems, but ASI remains speculative and timeline estimates are highly uncertain.theaireport+2

Where we are now

Current frontier models show impressive gains in coding, reasoning benchmarks, and multimodal tasks, and some can already write and improve their own software in constrained settings.scientificamerican+1

However, these systems still fail in robust general reasoning, long‑horizon planning, and reliable self‑improvement—capabilities most definitions of AGI or ASI would require.hai.stanford+1

So the field is in a phase of “advanced but brittle” systems, not in sight of true superintelligence.

Expert timelines and disagreement

Recent expert surveys put the median 50% probability for AGI sometime between roughly 2040 and 2061, though a vocal minority predicts much earlier dates.forbes+1

Some commentators then assume a relatively fast transition from AGI to ASI, with speculative ranges from a few years to several decades; one analysis frames a “useful estimate” of about 10 years from AGI to ASI.theaireport+1

At the same time, many experts (around three‑quarters in one survey) think simply scaling today’s techniques is not enough for AGI, let alone ASI.theaireport

Indicators of movement toward ASI

Rapid capability scaling: Benchmarks show steep year‑on‑year jumps in areas like multimodal understanding and software engineering, plus large drops in compute cost for a given capability level.hai.stanford+1

Early self‑improvement: Leading models can already optimize their own code or assist in model design, raising the question of whether this could ever “snowball” into open‑ended self‑improvement.scientificamerican+1

These trends are why some researchers argue we might be seeing the first steps toward systems that could one day underpin superintelligence, even if that point is still far away.scientificamerican

Cautious views and roadmaps

Researchers like Yann LeCun emphasize that even ambitious roadmaps aiming at “advanced machine intelligence” still expect only animal‑level world understanding (e.g., “cat or rat” level) prototypes within a few years, not human‑ or super‑human minds.eetimes

Groups branding themselves around “ASI” publish roadmaps that explicitly admit human‑level AGI has not yet been reached and present ASI as a longer‑term goal after major research advances.superintelligence

These more conservative views highlight that achieving robust world models, reasoning, and planning is still an unsolved problem.

How near are we, realistically?

No ASI today: There are no systems that fit the common definition of intelligence vastly beyond the best human experts across all domains.theaireport+1

AGI first, ASI later (if at all): Most structured analyses treat ASI as contingent on first achieving AGI, with a further uncertain period—possibly years to decades—before any superintelligent phase.forbes+1

Taken together, a reasonable reading of the evidence is: ASI is not imminent, serious people disagree on whether it is this‑century or ever, and the main near‑term focus is on managing rapidly strengthening but still fallible AI systems rather than on a concrete ASI arrival date.hai.stanford+2

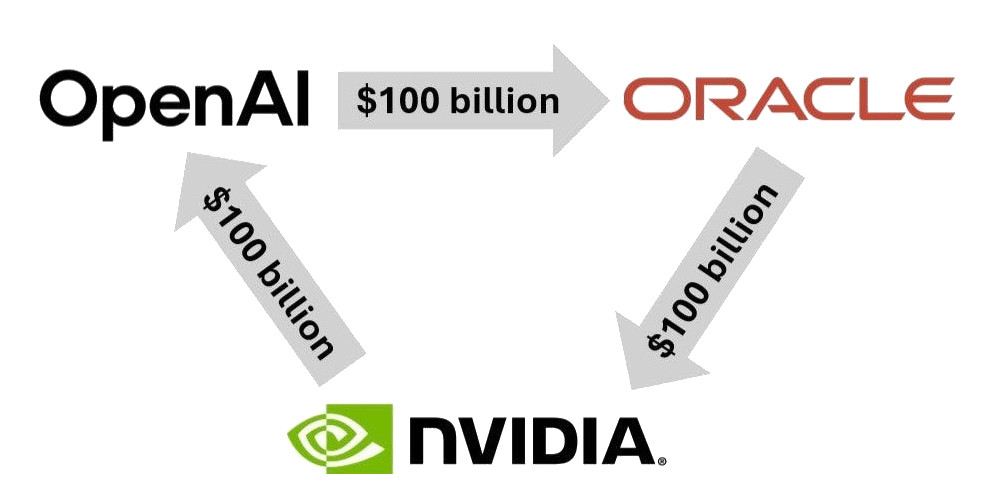

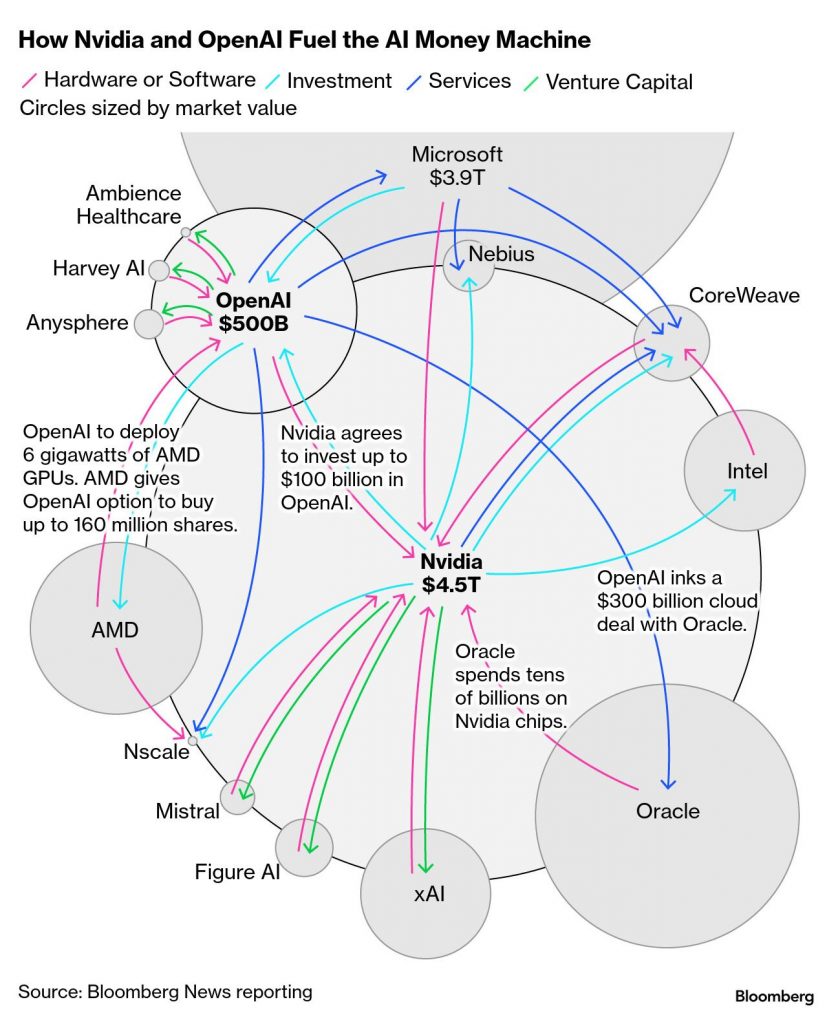

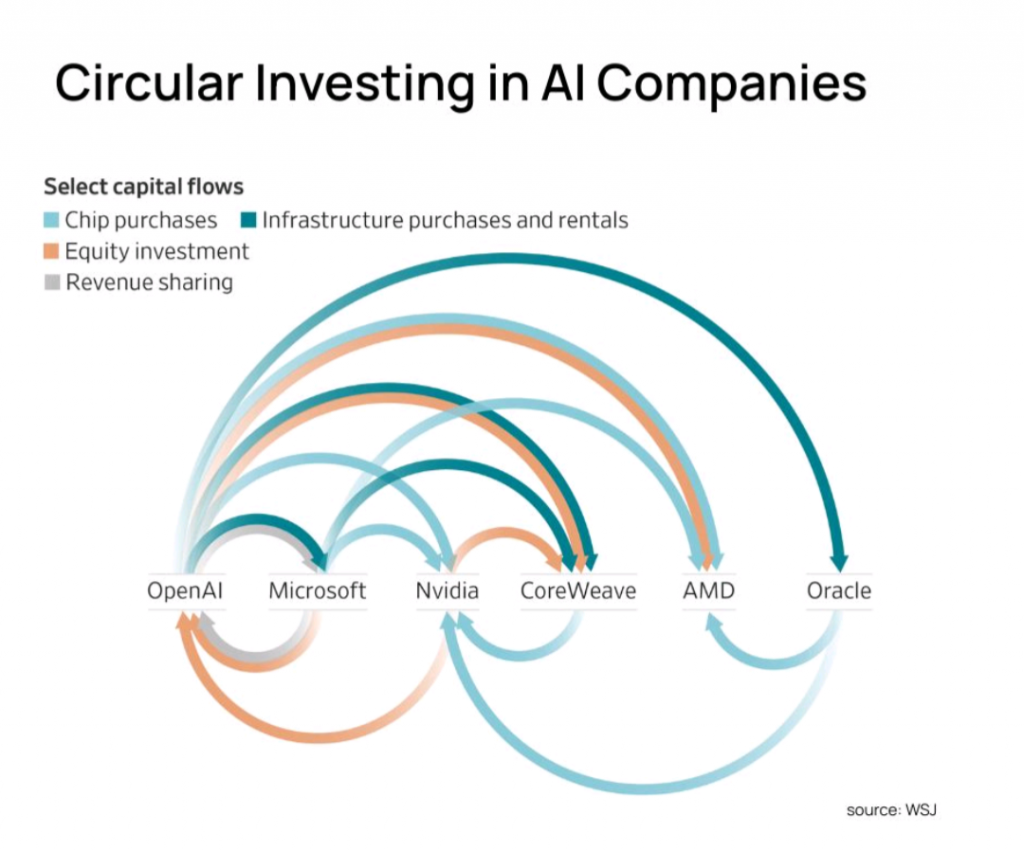

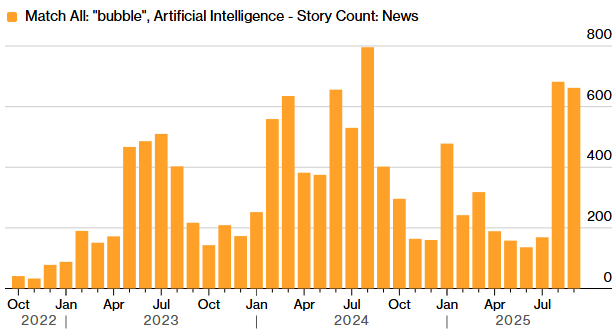

We’ve all seen the above image when Oracle started making waves about their AI contract to provide OpenAI compute power at their Abilene DC with tonnes of NVIDIA GPUs – well there’s now news about circular financing fraud involving the big AI players…

We look at what this article is saying and assess whether a postive circular financing fraud case will be the pin that bursts the AI bubble: https://substack.com/home/post/p-179453867

The article describes how advanced trading algorithms and machine intelligence detected an unprecedented $610 billion circular financing fraud involving major AI industry players, including Nvidia, Microsoft, OpenAI, Oracle, and xAI. This scheme involved companies repeatedly recycling the same money through chip purchases, cloud credits, and investments, allowing them to recognize fictitious revenue and inflate financial numbers without actual cash being exchanged.binance+3

What Happened

On November 20, 2025, AI-driven trading systems analyzed Nvidia’s earnings and discovered massive inconsistencies: billions in accounts receivable remained unpaid, and customers were taking longer to pay, resulting in aging bills and swelling inventories. The investigation revealed funds circulated between firms—such as Nvidia investing in xAI, which would use pushed loans to buy Nvidia chips, while Microsoft and Oracle funneled cloud credits through OpenAI—getting booked as revenue at multiple companies, but with no real payment behind the transactions.instagram+2

Impact on Financial Markets

Once the fraud was flagged, Nvidia’s stock, which had surged by $130 billion after earnings, quickly crashed as algorithms triggered selloffs faster than human analysts could respond. Bitcoin, used by many AI startups as loan collateral, also plunged as market confidence evaporated, with experts predicting further Bitcoin sell-offs as defaults increase.stockmarketanalysis04.substack+2

Industry Reactions and Fallout

Executives—including those from Airbnb and OpenAI—acknowledged the reliance on artificial “vibe revenue,” admitting the industry’s expected future profits were vastly overstated, and many projects would never deliver the anticipated returns. Famous investors quickly exited positions, and credit agencies are expected to downgrade the sector as payment cycles lengthen and the circular financing unwinds.news.futunn+2

Warnings and Criticism

Analysis of the reports cautioned that while some claims align with public financial data, other details appear speculative or exaggerated, casting doubt on the scale and specifics of the fraud presented in the article. However, the exposure of circular accounting practices has sparked renewed scrutiny of AI industry finances and the systemic risks they pose to both tech and broader financial markets.x+1

What would be the market implications if the fraud is confirmed?

If the $610 billion AI industry fraud is confirmed, the market implications would likely be severe and multifaceted:

Stock prices of the companies involved would likely experience sharp declines, similar to historic fraud cases where stock prices dropped significantly upon fraud discovery and investigation announcements. For example, firms have seen cumulative abnormal returns fall by 29% at fraud discovery and further 8% after regulatory investigation announcements, particularly when fraud involves revenue recognition or asset overstatement.nacva+1

Investor trust across the AI and related tech sectors would erode drastically, causing not only plummeting stock demand for the implicated companies but also collateral damage to wider market confidence. This loss of trust can depress sales, revenue, and overall financial performance beyond the direct fraud perpetrators.financemagnates

Increased regulatory scrutiny and enforcement actions would follow, including potential SEC investigations, fines, and legal consequences for perpetrators, shaking market stability and inviting tighter oversight on AI industry financial reporting.fraud+1

The revelation of such a large-scale circular financing scheme would raise concerns over information opacity and systemic risks in the AI sector and adjacent markets. This could raise the risk of future stock price crashes and long-term market volatility due to shaken investor confidence and greater caution toward AI-related investments.sciencedirect

Credit downgrades and withdrawal of investment capital across affected companies and startups would likely accelerate, hampering innovation financing and causing a sector-wide funding crunch.binance

Together, these effects imply a potential market shock comparable to major corporate fraud scandals, with profound short-to-medium term disruptions in AI industry valuations and investor behavior, and increased regulatory and due diligence focus on AI sector financial transparency.nacva+2

Which peer firms and sectors would face contagion risk?

If the $610 billion AI industry fraud is confirmed, the peer firms and sectors facing contagion risk would include:

Other major AI and technology firms interconnected via investments, chip sales, and cloud services, such as Microsoft, Oracle, OpenAI, and Nvidia’s competitors. Because the fraud involved circular financing among these players, their financial health and market valuations would be at risk of contagion through direct exposures and reputational damage.

The broader technology sector, including semiconductor manufacturers, cloud infrastructure providers, and AI startups, which depend heavily on investment flows and customer confidence linked to the implicated firms. Funding shortages and tighter credit conditions would ripple across these linked companies.

Financial institutions such as banks, investment funds, hedge funds, and insurers holding equity, debt, or derivatives tied to AI and tech firms. Market shocks from the fraud revelation could trigger liquidity strains, asset fire sales, and valuation drops across these financial intermediaries.

Sectors with strong dependence on AI-driven growth or technology investments, including software service companies, cloud computing, and innovative tech hardware industries, which would face heightened volatility and funding risks from cascading investor withdrawals.

In summary, the contagion risk would span a network of interlinked AI/tech firms, their financial backers (banks, funds, insurers), and adjacent sectors relying on AI-driven growth and innovation capital. These risks would be amplified by dense financial linkages, cross-holdings, and overlapping investor exposure, potentially escalating systemic risks and market instability across these interwoven sectors.ecb.europa+2

How likely is this a fraud?

The likelihood of this $610 billion AI industry fraud being real appears mixed, with some evidence supporting concerns but also significant skepticism about the full scale and details.

Support for fraud possibility: Automated algorithms detected unusual circular financing flows and discrepancies in accounts receivable, payments, and inventory levels among key players like Nvidia, OpenAI, Microsoft, and Oracle. Executives and industry insiders have acknowledged artificial revenue recognition practices, “vibe revenue,” and unsustainable burn rates, fueling suspicions of inflated financial reporting and reliance on self-referential capital cycling.reddit+2

Skepticism: Several data points in the original fraud claim articles do not fully align with official financial statements or audited reports. For example, some growth rates and cash conversion claims appear unverified or exaggerated, and robust revenue projections remain in place for major firms like Nvidia. Critiques suggest parts of the narrative may be speculative or amplified to support short-selling or competitive narratives.news.futunn+1

Market actions such as large insider sales, stock volatility, and algorithmic trading responses reflect real concerns but do not alone prove deliberate fraud.

Overall, while there is credible reason for regulatory scrutiny and investor caution, it is not yet conclusively proven that a $610 billion-scale fraud has occurred as portrayed. Financial markets and regulators will need to conduct thorough audits and investigations to confirm or refute the full extent of circular financing and unverifiable revenues in the AI sector.reddit+1

What additional evidence would confirm or refute the fraud claim?

To confirm or refute the $610 billion AI industry fraud claim, the following additional evidence would be critical:

Detailed audit reports and forensic accounting analyses that reveal whether reported revenues and assets align with actual cash flows, eliminating circular financing and fictitious transactions. Clear documentation of payment trails and verification of accounts receivable would be vital.

Access to internal communications, contracts, emails, and loan agreements showing intent, knowledge, or concealment of fraudulent practices among the companies involved. These would demonstrate deliberate misrepresentation rather than innocent errors.

Independent verification of inventories, customer payments, and cloud credit usage that purport to back financial figures, to detect any discrepancies or inflated valuations.

Testimonies or whistleblower accounts from insiders who can provide direct evidence of deception, revenue manipulation, or artificially inflated accounts.

Examination of algorithmic data and trading patterns that initially flagged the fraud, corroborated by hard financial evidence to remove speculation.

Legal scrutiny and regulatory investigations with power to compel document production and testimony, leading to formal findings of fraud based on a balance of probabilities.

These types of evidence collectively would build a persuasive case by proving the key elements of fraud: false statements of fact, knowledge of falsity, intent to deceive, reliance on the falsehood by others, and resulting financial damage.lincolnandrowe+3

Due to the big players involved, how like is this to be recognised as fraud?

Given the involvement of major public companies such as Nvidia, Microsoft, Oracle, and OpenAI, it is relatively less likely that the alleged $610 billion circular financing scheme would go unrecognized or uninvestigated by regulators, auditors, and independent analysts. These firms operate under strict financial reporting standards, are subject to continuous market scrutiny, and have audits performed by reputable firms. Nvidia, for example, is audited by PwC and rated highly by credit agencies, and recently reported strong revenue guidance despite allegations.news.futunn+1

However, the complexity and scale of circular financing and vendor financing deals—spread across multiple firms and private entities like OpenAI—and the extraordinary sums involved create challenges in transparency. Given the high stakes, any material misstatements or abuses would likely draw regulatory attention from bodies like the SEC, and investigations would follow, as evidenced by past fraud cases in tech and finance.peterwildeford.substack

Market reactions such as rapid stock sell-offs, insider selling, and investor withdrawals suggest heightened suspicion and the potential for increased scrutiny. But actual recognition of fraud depends on whether clear evidence emerges proving intent and knowing misrepresentation, beyond complex but possibly legitimate financial engineering.substack+1

Therefore, while these large players’ reputations, audit requirements, and regulator oversight make outright fraud recognition more probable than in less regulated sectors, proving the full scope involves thorough forensic audits and investigations. The high-profile nature ensures any verified fraud will be highly publicized and swiftly acted upon.tomtunguz+3

The public seems to be able to see this circular financing already, but there has been no obvious denies or evidence until now?

The public’s ability to observe the circular financing is likely due to the following:

Many of the so-called circular financing deals in AI are part of legitimate strategic partnerships, vendor financing, and ecosystem-building efforts. Companies like Nvidia, OpenAI, Microsoft, AMD, Broadcom, and others are deeply intertwined financially and operationally, investing heavily in each other through chip sales, equity stakes, and cloud infrastructure deals. This creates a “circular economy” that keeps capital flowing within a compact network, which is visible in market disclosures and company announcements but can appear as circular funding to outside observers.forbes+2

These circular arrangements often reflect business models designed to ensure long-term demand for AI hardware and cloud services while fostering innovation through close alliances. While they may inflate revenue temporarily on paper by recognizing sales within the network, such practices are also common vendor financing strategies used in many industries historically and are not necessarily fraudulent if transparently disclosed and compliant with accounting standards.reddit+1

Until now, there has been no obvious denial or strong rebuttal partly because companies benefit from these arrangements to drive AI ecosystem growth and financial performance, and the accounting treatments remain within legal frameworks. The lack of clear external evidence against them also means regulators and auditors have not formally challenged these practices as fraudulent yet, despite increasing scrutiny and skepticism among investors and algorithms detecting anomalies.bbc+1

The recent algorithmic detection of potential fraud has heightened attention and raised the stakes for transparency, but distinguishing aggressive vendor financing from deliberate fraud requires detailed forensic audit evidence and regulatory investigation.

Thus, the public is seeing signals of circular financing because it is foundational to how AI ecosystem finance currently operates, but formal fraud recognition demands deeper proof beyond visible financial flows circulating within interconnected big players.ubs+3

There isn’t going to be a single answer to why we are experiencing major global internet outages of late. There will be a number of reasons that are all coinciding to produce these recent occurrences.

Recognising these reasons will allow us to predict who is next after AWS, Azure and Cloudflare…

Why is today’s internet so fragile?

Recent outages at AWS, Azure, and Cloudflare have starkly exposed just how fragile today’s internet is, largely due to concentrated infrastructure, dependency on a handful of providers, and architectural choices that allow minor failures to trigger global disruptions.gulfnews+2

Extreme Centralization

The internet now relies heavily on a few “invisible” giants: AWS, Azure, Google Cloud, and Cloudflare together account for most global web traffic, hosting, routing, and security.techwireasia+1

Cloudflare alone accelerates and protects an estimated 20% of all internet traffic. When any of these services experience issues, disruption ripples across thousands of companies and billions of users, as seen in recent events.computing+1

Cascading Failures

Outages often start with technical errors such as DNS failures, network misconfigurations, or buggy software updates. Because so many services are built on top of these platforms, a seemingly small incident can snowball rapidly into crippling downtime across the world.modern-networks+1

For example, a DNS outage at AWS led to millions of user lockouts and stalled applications globally, while Cloudflare’s recent bug knocked out platforms like ChatGPT, X (Twitter), Spotify, and many SaaS tools all at once.deployflow+2

Lack of True Redundancy

While cloud vendors offer robustness at the hardware and software level, many applications and businesses still depend on single providers or even single cloud regions, lacking the architectural redundancy needed for true resilience.cnn+1

Multi-cloud designs are promoted as a solution, but adoption remains slow due to complexity and cost.economictimes+1

Legacy Internet Foundations

Critical protocols like DNS, which translate website names to machine addresses, are based on decades-old designs. If DNS fails at a major provider, or a bad configuration is cached globally, the effects can take hours or even days to fully resolve.techwireasia+1

Economic and Societal Risk

Because core digital payments, communications, and business tools are now web-based, cloud outages don’t just inconvenience consumers—they can disrupt financial markets, logistics, healthcare, and government.itbrief+1

Governments are beginning to treat cloud and network resilience as matters of national security, pushing for failover planning and measures against systemic risk.gulfnews+1

Driving the Future

These outages are accelerating moves to adopt decentralized architectures (Web3), distributed CDNs, and alternatives to centralized cloud platforms.gulfnews

Still, until broad and real decentralization is achieved, today’s internet remains vulnerable to concentrated points of failure—making global web fragility an ongoing and deeply technical challenge.cnn+1

Is the complexity of modern software, apps and services that make the internet brittle?

There is strong, concrete evidence that the rising complexity of software, applications, and IT services is directly making the internet more brittle and increasingly prone to outages.uptimeinstitute+2

How Complexity Drives Fragility

Modern applications are built on tightly interdependent components, microservices, APIs, and SaaS layers. Even minor changes—like a configuration tweak or a faulty software update—can cascade through interconnected systems, causing large-scale outages.ashrafmageed+1

Real-world outages, such as the infamous Facebook, AWS, and Azure disruptions, have repeatedly been traced back to software bugs, unexpected side effects between services, or misconfigurations in complex control planes.thousandeyes+1

Concrete Examples

The October 2021 Facebook outage resulted from a misconfiguration update that propagated through its global BGP (Border Gateway Protocol) infrastructure, causing a full disconnection from the internet—demonstrating how internal software complexity can have massive external effects.theintelligraph

The 2020 Azure and recent AWS outages were triggered by subtle software bugs or missteps in automated update pipelines. What began as isolated technical errors quickly led to global knock-on effects due to hidden dependencies and insufficient isolation between services.thousandeyes+1

The CrowdStrike security software update in 2024 caused mass Windows system crashes and “bootloops,” showing how a flaw in widely deployed software had a systemic effect far beyond one organization.news.exeter

Industry Data and Research

Reports from Uptime Institute and industry observers state that software, network, and configuration issues—many stemming from growing complexity—are the fastest-growing sources of critical IT outages. As architectures shift to the cloud, hybrid or multi-cloud forms, and “infrastructure as code,” the number of places where failure can originate multiplies.securitybrief+1

Complexity makes it harder for engineers to fully understand the system, increasing cognitive load. Documentation may lag, tests are often brittle, and adding new features or changing existing code can unintentionally break other parts of the stack, amplifying the risk of downtime.codurance+1

In Summary

Concrete evidence from industry reports, postmortems, and technical analyses shows that software and architectural complexity is now a leading cause of major outages across the internet and digital services.uptimeinstitute+2

As IT services and software systems become ever more entangled, even small mistakes or bugs can propagate, causing widespread disruption and emphasizing the need for simplicity, redundancy, and rigorous testing in critical systems.theintelligraph+1

The third reason for internet outages being more common and prevalent in the modern age

A third major reason internet outages are more common in the modern age is the increased frequency and sophistication of cyberattacks, including ransomware and targeted digital assaults on critical infrastructure.datacenter.uptimeinstitute+2

Cybersecurity Threats and Ransomware

Recent years have seen a rapid rise in outages caused by cyberattacks, especially ransomware campaigns and distributed denial-of-service (DDoS) attacks targeting cloud providers, SaaS platforms, and essential network infrastructure.telconews+1

These attacks can disable services, corrupt data, and sometimes require shutting down affected systems entirely for forensic investigation and restoration.datacenter.uptimeinstitute

As much as the physical and software layers have become more complex, new vulnerabilities are constantly emerging, and attackers exploit these with increasing speed and precision, making outages both more frequent and severe.teridion+1

Why This Is Rising

Greater digital transformation and cloud adoption have made critical services attractive and lucrative targets for cybercriminals.telconews+1

Even well-secured organizations are vulnerable to supply-chain attacks—where the compromise of a key vendor or upstream software provider can cascade globally and impact hundreds or thousands of customers at once.datacenter.uptimeinstitute

Research and industry analyses show that successful large-scale ransomware and cyber incidents are now among the leading triggers of major public outages, alongside centralization and complexity.telconews+1

In summary, cyberattacks—especially ransomware—represent a third key factor making internet outages more prevalent and impactful in the modern era, adding to the fragility created by centralization and increasing system complexity.teridion+2

Who will have the next outage that will affect the global internet?

Based on current evidence and industry analysis, the next global internet outage is most likely to be triggered by one of two sources: either a failure at a major cloud or infrastructure provider due to software or configuration errors, or a cyberattack targeting critical cloud services or undersea cables. However, there is also significant expert concern that a severe solar storm during the predicted Solar Maximum in 2025 could cause even wider disruption by damaging undersea cables and global communication infrastructure.financialexpress+2

Most Direct Triggers

Cloud Provider Error: Given recent patterns, a chain reaction sparked by a misconfiguration, flawed software update, or unexpected cascade within AWS, Azure, Google Cloud, or Cloudflare remains the most likely culprit for another major outage. The interconnected nature of cloud services means a localized issue can propagate system-wide in minutes.thousandeyes+1

Cyberattack: Large-scale, coordinated ransomware or DDoS campaigns are rising and present a considerable threat. Critical SaaS, CDN, and DNS infrastructure are prime targets. A breach in a major provider or a critical software library could affect thousands of businesses globally at once.reports.weforum+1

Solar Storm Risk

Solar Maximum 2025: Some experts now warn that natural events—specifically powerful solar storms—could damage undersea fiber links and data centers, causing internet outages far more widespread and unpredictable than anything to date. While rare, the impact could last for days or even months, with recovery depending on the ability to repair undersea infrastructure and restore communications.cnbctv18+1

Unpredictable Factors

It’s increasingly difficult to forecast who or what will cause the next global outage because architectures are more complex, attack surfaces are broader, and even well-intentioned updates or external environmental events can have devastating consequences.financialexpress+1

In summary, the next global internet outage is most likely to be created by a technical failure or attack affecting critical infrastructure (cloud, DNS, CDN), but severe space weather disruptions are also being seriously considered by experts for 2025.cloudflare+2

Among GCP (Google Cloud Platform), Broadcom, Oracle, IBM, Meta, and Apple, GCP carries the highest risk of causing the next global internet outage. This is due to its position as a major cloud service provider, with deep integration into SaaS, enterprise infrastructure, APIs, and many consumer services. Outages from cloud providers frequently propagate to thousands of dependent services and users worldwide, amplifying systemic impacts.insuranceinsider

Why GCP Is Most Likely

Cloud providers pose systemic risk because centralized cloud infrastructure hosts, manages, and routes massive portions of the world’s internet traffic.cybcube+1

GCP, while smaller than AWS and Azure, still represents a major aggregation point: it powers business-critical workloads (banking, retail, logistics), hosts thousands of SaaS platforms, and provides back-end APIs for many mobile apps and connected devices.insuranceinsider

Recent cloud incidents (AWS, Azure, Cloudflare) have proven how failures in authentication, DNS, or network configuration can quickly cascade to global impact, and GCP’s technical complexity and interconnections make it vulnerable to similar risks.piranirisk+1

Risk Assessment of Others

Broadcom: While it designs key hardware and networking gear, it is less likely to directly trigger a software or routing-linked global outage at internet scale. Its risks are supply-chain and chip-related, not service aggregation.carnegieendowment

Oracle, IBM: Both power significant enterprise IT, but they are not primary cloud or content routing platforms for consumer web services. Oracle Cloud is growing but has not reached the single-point-of-failure scale of GCP or AWS.insuranceinsider

Meta, Apple: Outages from these can severely disrupt social media or device ecosystems, but they do not underlie the broad global infrastructure dependencies typical of a cloud provider failure.carnegieendowment

Industry Consensus

Reports and regulators consistently identify major cloud providers as critical “single points of failure.” When cloud aggregation, concentration, and technical complexity are considered, GCP ranks highest within your list for systemic outage risk.cybcube+1

In summary, GCP is the most likely among your choices to trigger the next global-scale outage, because cloud providers are at the heart of internet infrastructure and software dependencies today.cybcube+1

It is no secret that I am leaving Oracle to join Nscale at the end of this month. My main aim was to avoid the Oracle RIF/layoffs and while putting the worse case scenario in place, I managed to get a role at Nscale.

Both Oracle and Nscale are hedging their bets on AI and with the current worry that the AI bubble is going to burst, with the boss of Google saying: ‘no company is going to be immune’ [BBC], I asked AI these questions…

How Oracle would suffer in an AI crash?

Oracle would experience significant financial and operational setbacks if an AI crash occurs, mainly because its recent strategy has focused heavily on AI cloud infrastructure and hyperscaler partnerships. Here’s how Oracle and Oracle Cloud Infrastructure (OCI) would suffer:

Revenue Slowdown and Underutilized Data Centers

Oracle expects that AI-driven cloud infrastructure could make up the majority of its revenue by 2030, with multi-billion dollar GPU investments and flagship deals supporting OpenAI, Meta, and other hyperscale model trainers.webpronews+1

In an AI crash, client demand for large-scale training and inference workloads would sharply decline. That means Oracle’s new data centers and GPU fleets (including hundreds of thousands of Nvidia GPUs) could become underutilized, forcing write-downs and lowering ROI.fortune

Margin Compression and Volatility

Oracle’s current margins on AI cloud offerings are modest (around 14% in recent quarters), and plans for improvement depend on scale and full utilization of infrastructure.bloomberg+1

Reduced client activity would keep margins low or negative, intensifying investor scrutiny and driving downward pressure on stock price—recent volatility already shows concern over fulfilling ambitious AI cloud predictions.cnbc+1

Oracle would also struggle to justify continued massive investments to shareholders if growth fails to materialize.

Exposure to Contract and Customer Risk

Oracle is especially exposed to a few large anchor clients (e.g. OpenAI, Microsoft), who may defer or downsize contracts if the economics of large-model training weaken.webpronews+1

Cancellations or renegotiations on these hyperscale deals would lead to revenue instability and possible reputational harm in the cloud sector.

Delayed Application Growth and Broader Impact

While Oracle’s core application business (ERP, NetSuite, traditional cloud services) offers some revenue buffer, these divisions would also be affected by a broader tech and enterprise spending slowdown typical in an AI-induced market downturn.constellationr+1

Expansion plans and R&D investment would likely be scaled back, slowing Oracle’s ability to compete with more insulated rivals.

Summary Table: Oracle’s Pain Points in an AI Crash

Effect Area

Oracle Cloud & Business Impact

Infrastructure ROI

Underutilized data centers, GPU fleets

Margins & Profit

Margin compression, stock volatility

Contract Risk

Deferred/canceled hyperscale projects

App/Enterprise Spend

Revenue dampening, slower growth

In summary, Oracle would suffer via underperforming cloud assets, margin pressure, dependency on a handful of high-risk AI clients, and contraction of enterprise demand. While traditional non-AI applications offer some shelter, the scale of Oracle’s recent AI cloud bets makes it highly exposed to a major market correction.reuters+6

How Nscale would be affected by an AI crash?

Nscale would be severely affected by an AI crash due to its intense reliance on hyperscaler contracts, rapid capital deployment, and debt-financed AI infrastructure builds. Its business model is specifically geared toward serving large-scale AI model training and compute workloads, making it one of the highest-risk startups in a downturn scenario.

Revenue Freeze and Stranded AI Data Centers

If AI demand collapses, hyperscalers like Microsoft and OpenAI—Nscale’s anchor clients—would scale back their contracts, delay GPU purchases, or walk away from expansion phases, freezing Nscale’s main cashflow pipeline.computing

Data centers built for intensive model training could be left mostly idle, forcing Nscale to absorb heavy operational losses while continuing to service debt and lease obligations.

Investor and Debt Pressure

Nscale’s recent $1.1 billion Series B and $433 million SAFE financing involve a mix of industrial and venture capital (Aker, Nvidia, Dell, Blue Owl), and depend on optimistic growth projections and future contract fulfillment.cnbc+3

In a crash, these investors would likely mark down their stakes significantly, making further fundraising difficult. If cash flow dries up, Nscale could face covenant breaches, mass layoffs, and possibly insolvency.

Asset Write-Downs and Market Value Declines

Large inventories of Nvidia GPUs and purpose-built data centers for AI workloads could lose much of their resale value if a flood of surplus infrastructure hits the market simultaneously.computing

Hardware and campuses not suited for general-purpose workloads would be especially vulnerable—mirroring the fate of unused “dark fiber” and crypto-mining assets after previous speculative bubbles burst.

Strategic Pivot and Survival Pathways

With deep exposure to hyperscaler deals, Nscale’s best shot at survival would be pivoting toward government-backed sovereign compute projects, or repositioning under-utilized capacity for scientific, academic, or inference-driven workloads.computing

However, the overall scale-back in AI investment would make even these pivots challenging and may require restructuring, asset sales, or merger activity.

Summary Table: Nscale’s Crash Exposure

Pain Point

Crash Impact

AI contract reliance

Revenue freeze, phased-out deals, layoffs

Infrastructure assets

Write-downs, idle data centers, GPU oversupply

Investor relations

Markdowns, covenant risk, fundraising difficulty

Pivot opportunities

Limited to sovereign or non-AI workloads

In summary, Nscale would be among the hardest-hit AI infrastructure startups during a crash, facing immediate cash flow problems, asset devaluation, and existential threats unless it rapidly adapts or receives protective strategic support.uktech+4

As an employee of Oracle or Nscale – who would be worst affected in an AI crash?

As an employee, Nscale staff would likely be much worse affected by an AI crash than Oracle employees. This is due to the relative scale, business diversity, and risk tolerance of the two companies:

Nscale Employees: High Risk

Startup Vulnerability: Nscale is a high-growth, venture-backed startup focused almost entirely on the AI cloud hyperscaler market. If an AI crash occurs, Nscale would face abrupt revenue freezes, contract withdrawals, and rapid asset devaluation, with far less financial cushion to weather losses than a large incumbent like Oracle.

Layoffs and Insolvency Risk: In a crash, Nscale may be forced to lay off a substantial portion of its workforce quickly, pause projects, or even enter administration if funding evaporates or debts cannot be serviced. Employees could face sudden job loss, delayed salaries, and loss of equity value, with fewer internal opportunities for reassignment.

Equity and Options: Most compensation upside for Nscale staff is likely tied to startup equity. A market correction would deeply devalue or wipe out employee options/shareholdings, and prospects for another lucrative exit (e.g., IPO or acquisition) would diminish drastically.

Oracle Employees: More Stability, Less Immediate Risk

Diversified Business: Oracle is a global enterprise with diversified revenue streams across cloud, applications, hardware, licensing, and services. Even with heavy AI investment, its overall risk is spread out, and core business lines would remain resilient.

Less Severe Layoffs: Large tech companies like Oracle do enact layoffs in downturns, but they tend to be more measured and spread across divisions. Employees have more options to transfer internally or leverage severance and career support programs.

Compensation Impact: Public company employees with RSUs or stock options would feel a drop in value, but these tend to recover after corrections, and overall job security remains higher due to Oracle’s operational scale and financial reserves.

Summary Table

Factor

Nscale Employee Impact

Oracle Employee Impact

Layoff risk

Extremely high, abrupt

Moderate, measured

Job security

Low

High

Equity/option value

Likely wiped out

Lower, but more resilient

Internal mobility

Minimal

Significant

Corporate backup/support

Minimal/none

Substantial

In summary: Nscale employees are far more exposed to job loss, equity wipeout, and uncertainty during an AI crash, while Oracle employees—even in affected AI-focused roles—would generally be shielded by the company’s size, global reach, and business diversity.

What is the benefits of joining Nscale for my career over staying at Oracle

Joining Nscale instead of staying at Oracle offers a profoundly different set of career benefits and risks. Your choice should be shaped by your appetite for growth, impact, compensation profile, and risk tolerance.

Career Acceleration and Impact

Rapid Responsibility & Visibility: At Nscale, a high-growth AI infrastructure startup, you’re likely to hold broader responsibilities, have a direct line to executives, and see tangible impact from your contributions—versus a more specialized, hierarchical environment at Oracle.linkedin+1

Cutting-Edge Technology Exposure: Nscale’s business is centered around the latest in AI hyperscale, GPU clusters, and sovereign compute, putting you at the heart of Europe’s most ambitious AI and cloud projects. This hands-on work accelerates technical learning and keeps you current with elite tooling.linkedin

Networking Opportunity: Being at a much talked-about scaleup, you’ll interact with top-tier industry partners (Microsoft, Nvidia, blue-chip VCs), as well as the fast-moving European AI ecosystem, which can boost professional reputation and future opportunities.cnbc+1

Compensation and Equity

Equity Upside: As with most startups, joining Nscale comes with employee equity—potentially life-changing financial upside if the company’s rapid growth leads to a successful IPO or acquisition. At Oracle, equity is usually granted as RSUs whose upside, while substantial, is tied to a mature company’s slower growth trajectory.

Compensation Mix Changes: Startup salary may be lower or matched to Oracle’s, but total comp potential is usually tied more to company performance and exit events.

Innovation, Learning and Influence

Innovation Environment: Nscale’s pace and hunger for innovation generally surpass what’s possible at a large, diversified incumbent like Oracle. Progression can be much faster for high performers at a startup, and you have more say in technical and strategic direction.

Learning Curve: The breadth of challenges—from scaling infra to winning deals and iterating products for hyperscaler clients—means you’ll develop skills quickly that are valuable for future founding roles, CTO posts, or senior technical leadership.

Risks, Trade-Offs and Stability

Job and Financial Risk: As shown in your AI crash scenario queries, Nscale is exposed to sector volatility. Layoff, equity wipeout, or strategic pivots are real risks in a downturn, while Oracle offers much greater job security and stable, long-term career pathways.

Work-Life Balance: Startups typically expect longer hours and intense focus, often trading stability for the chance at rapid advancement and financial gain.

Summary Table: Nscale vs Oracle Career Benefits

Career Factor

Nscale (Startup)

Oracle (Enterprise)

Career acceleration

Very high—fast progression, impact

Slower, more structured

Tech exposure

Latest/bleeding-edge AI/GPU work

Solid, broad enterprise stack

Compensation upside

High equity, risky

Stable salary, predictable RSUs

Job security

Low—volatile, high layoff risk

High, robust to market downturns

Influence

Large, direct access to leadership

Smaller, part of larger organization

Work-life balance

Often demanding

Generally more moderate

Networking

Top-tier VCs, hyperscalers, founders

Global enterprise contacts

In summary: Nscale offers a “rocket ship” growth and learning environment for someone hungry for ownership, innovation, and possible equity windfall—but this comes with higher risk and volatility. Oracle provides greater long-term job security, measured career progression, and reliable compensation, but less potential upside and less direct influence. The right choice depends on your risk appetite, ambition, and career goals.uktech+2

An AI crash would resemble a hybrid of the 1990s dot-com bust and the 2008 financial crisis—but centered around artificial intelligence infrastructure, data centers, and corporate overinvestment. It would likely begin as a sudden market correction in overvalued AI firms and GPU suppliers, then spread through the financial system and tech economy as debt and demand collapse.

Market and Investment Collapse

In early stages, overleveraged companies like OpenAI, Anthropic, or firms heavily reliant on GPU compute (e.g., Nvidia, Oracle, Microsoft) would face sharp valuation drops as AI-generated revenues fail to justify trillion-dollar capital expenditures. Investor panic could trigger a chain reaction, collapsing the leveraged network of data‑center finance. Bloomberg and the Bank of England have both warned of a “sudden correction” and circular investing between chip firms and hyperscalers that artificially props up earnings.transformernews+1

The Data Center Bust

According to historian Margaret O’Mara and business analyst Shane Greenstein, AI data centers—many purpose‑built for model training using GPUs—are highly specialized and often remote from urban demand. These centers might last only 3–5 years and have little reuse value outside AI or crypto mining. If capital inflows freeze, thousands of megawatts of compute could become stranded assets, comparable to the empty fiber networks after the dot‑com collapse.transformernews

Economic Impact

The International Monetary Fund estimates roughly a third of current US GDP growth depends on AI-related investment. If the bubble bursts, consumption could fall from loss of “AI wealth effects,” dragging global markets into recession. Analysts at Transformer News liken it to Britain’s 1840s railway mania: vast sums invested in technology that ultimately enriched the future economy—at the cost of investors’ ruin.globalcapital+2

Consequences for Jobs and Technology

For the workforce, the crash would begin with mass layoffs across the tech sector and data‑center construction, followed by second‑order layoffs in software, marketing, and education technology. However, as with the post‑dot‑com era, redundant talent and abandoned infrastructure could later fuel a new, leaner AI industry based on sustainable business models.reddit+2

Systemic and Political Risks

While the contagion risk is smaller than subprime mortgages in 2008, debt-financed AI expansion—Oracle’s $100 billion borrowing plan with OpenAI being one example—creates vulnerability for lenders and investors. Should a major firm default, cascading insolvencies could ripple through the supply chain, forcing governments to intervene. Some analysts expect this crash would prompt stricter AI regulation and financing guardrails reminiscent of those enacted after the Great Depression.transformernews

Long-Term View

If artificial general intelligence (AGI) does eventually deliver major productivity gains, early investments may appear prescient. But if not, a 2020s AI crash would leave disused GPU campuses and massive debt—an exuberant experiment that accelerated technological progress at ruinous human cost.unherd+2

Which industries would collapse first in an AI crash

In the event of an AI crash, several sectors would be hit first and hardest — especially those that have overexpanded based on speculative expectations of AI-driven profits or infrastructure demand. The collapse would cascade through high-capex industries, ripple across financial services, and disrupt employment-dependent consumer sectors.

Semiconductor and GPU Manufacturing

The semiconductor industry would be the first to collapse due to its heavy dependence on AI demand. Data center GPUs currently drive over 90% of Nvidia’s server revenue, and the entire sector’s value nearly doubled between 2024 and 2025 based on AI compute growth forecasts. If hyperscaler demand dries up, the oversupply of GPUs, high-bandwidth memory (HBM), and AI ASICs could cause a price crash similar to the telecom equipment bust in 2002. Chip makers and startups like Groq, Cerebras, and Tenstorrent—heavily leveraged to AI workloads—would struggle to survive the sudden capital freeze.digitalisationworld

Cloud and Data Center Infrastructure

AI-heavy cloud providers such as Microsoft Azure, AWS, Google Cloud, and Oracle Cloud would see massive write-downs in data center assets. Overbuilt hyperscale and sovereign AI campuses could become stranded investments worth billions as training workloads decline and electricity costs remain high. This dynamic mirrors the way dark fiber networks from the 1990s dot-com era lay idle for years after overinvestment.digitalisationworld

Digital Advertising and Marketing

The advertising and media sector—already experiencing erosion due to AI‑generated content—would decline abruptly. Companies like WPP have already lost 50% of their stock value in 2025 due to automated ad-generation technologies cannibalizing human creative work. As AI content generation saturates the market, profit margins in marketing, online publishing, and synthetic media platforms like Shutterstock and Wix could collapse.ainvest

Financial and Staffing Services

Financial services and staffing firms are another early casualty. AI has already automated large portions of transaction processing, compliance, and manual recruitment. Firms such as ManpowerGroup and Robert Half have reportedly seen 30–50% market value declines due to these pressures. In an AI crash, their exposure to risk-laden corporate clients and shrinking demand for human labor matching would deepen losses, while regulators tighten AI governance in compliance-heavy finance.ainvest

Transportation and Logistics

The transportation and logistics sector, closely tied to AI investment through autonomous systems, faces structural weakness. Millions of driving and delivery jobs could disappear due to automation, but the firms funding autonomous fleets—such as Tesla Freight and Aurora Innovations—would hemorrhage cash if capital dries up before widespread profitability. AI‑powered routing and warehouse systems could be written down as expensive overcapacity.ainvest

Secondary Collapse: Retail and Customer Support

Finally, customer‑facing retail and support sectors would be heavily affected. With AI chatbots now handling about 80% of common queries, these labor markets are already contracting. A market shock would worsen layoffs while eroding spending power, compounding the downturn.ainvest

In short, the first phase of an AI crash would decimate GPU suppliers and infrastructure providers, followed by cascading losses in services and labor markets that relied on sustained AI adoption and speculative investor optimism.

The Hyperscalers who would be most affected in an AI crash

The hyperscalers most severely affected by an AI crash would be those that have sunk the largest capital into AI‑specific data center expansion without commensurate returns—primarily Microsoft, Amazon (AWS), Alphabet (Google Cloud), Meta, Oracle, and to a lesser extent GPU‑specialist partners like CoreWeave and Crusoe Energy Systems. These companies are deep in an investment cycle driven by trillion‑dollar valuations and multi‑gigawatt data center commitments, meaning a downturn would cripple balance sheets, strand assets, and force major write‑downs.

Microsoft

Microsoft is the hyperscaler most exposed to an AI collapse. It has committed $80 billion for fiscal 2025 to AI‑optimized data centers, largely to support OpenAI’s model training workloads on Azure. Over half this investment is in the U.S., focusing on high‑power, GPU‑dense facilities that may become stranded if demand for model training plunges. The company also co‑leads multi‑partner mega‑projects like Stargate, a $500 billion AI campus venture involving SoftBank and Oracle.ft+1

Amazon Web Services (AWS)

AWS is next in risk magnitude, with $86 billion in active AI infrastructure commitments spanning Indiana, Virginia, and Frankfurt. Many of its new campuses are dedicated to AI‑as‑a‑Service workloads and custom silicon (Trainium, Inferentia). If model‑training customers scale back, AWS faces overcapacity in power‑hungry clusters designed for sustained maximum utilization. Analysts warn that such facilities are difficult to repurpose for general cloud usage due to 10× higher rack power and cooling loads.thenetworkinstallers+1

Alphabet (Google Cloud)

Google’s parent company, Alphabet, has pledged around $75 billion in AI infrastructure spending in 2025 alone—heavily concentrated in server farms for Gemini model operations. The company’s shift to AI‑dense GPU clusters has already required ripping and rebuilding sites mid‑construction. In a crash, Alphabet’s reliance on advertising to subsidize capex would expose it to compounding financial stress.ft+1

Meta

Meta’s risk is driven by scale and ambition rather than cloud dependency. The company is investing $60–65 billion into a network of AI superclusters, including a 2 GW data center in Louisiana designed purely for model training. Mark Zuckerberg’s goal to reach “superintelligence” entails constant full‑load operation—meaning unused compute in a recession would yield enormous sunk‑cost losses.hanwhadatacenters+1

Oracle

Oracle, a late entrant to the hyperscaler race, ranks as the fourth largest hyperscaler and has become deeply tied to OpenAI’s infrastructure build. It is reportedly providing 400,000 Nvidia GPUs—worth about $40 billion—for OpenAI’s Texas and UAE campuses under the Stargate project. Oracle’s dependency on a few high‑risk customers makes it vulnerable to disproportionate collapse if those clients cut capital expenditures.ft

GPU Cloud Specialists (CoreWeave, Crusoe, Lambda)

Although smaller in scale, CoreWeave, Crusoe Energy Systems, and Lambda Labs face acute financial danger. Each is highly leveraged to GPU leasing economics that assume near‑continuous utilization. A pause in large‑model training would break their cash flow structure, causing defaults among the so‑called “neo‑cloud” providers.hanwhadatacenters

A sustained AI market collapse would first hit these hyperscalers through GPU underutilization, stranded data‑center capacity, and debt‑heavy infrastructure financing. Microsoft, Oracle, and Meta would face the most immediate write‑downs given their recent megaproject commitments. Amazon and Google, while financially stronger, would absorb heavy revenue compression. Specialized GPU‑cloud providers—CoreWeave, Crusoe, and Lambda—could fail outright due to funding constraints and dependence on short‑term AI demand surges.thenetworkinstallers+2

Hyperscalers are the giants of cloud computing — companies that design, build, and operate massive, global-scale data center infrastructures capable of scaling horizontally almost without limit. The term “hyperscale” refers to architectures that can efficiently handle extremely large and rapidly growing workloads, including AI training, inference, and data processing.

Examples:

Amazon Web Services (AWS)

Microsoft Azure

Google Cloud Platform (GCP)

Alibaba Cloud

Oracle Cloud Infrastructure (OCI) (smaller but sometimes included)

These companies have multi-billion-dollar capital expenditures (CAPEX) in data centers, networking, and custom hardware (e.g., AWS Inferentia, Google TPU, Azure Maia).

What Are Traditional AI Compute Cloud Providers?

These are smaller or more specialized providers that focus specifically on AI workloads—especially training and fine-tuning large models—often offering GPU or accelerator access, high-bandwidth networking, and lower latency setups.

Examples:

CoreWeave

Lambda Labs (Lambda Cloud)

Vast.ai

RunPod, Paperspace, FluidStack, etc.

They often use NVIDIA GPUs (H100, A100, RTX 4090, etc.) and emphasize cost-efficiency, flexibility, or performance for ML engineers and researchers.

Key Comparison: Hyperscalers vs. AI Compute Cloud Providers

Dimension

Hyperscalers

AI Compute Cloud Providers

Scale & Reach

Global, thousands of data centers; integrated with enterprise ecosystems

Simpler, often cheaper hourly or spot pricing; more transparent GPU pricing

Performance Focus

Balance of general-purpose and AI-specific workloads

Focused almost entirely on deep learning performance

Networking

Proprietary, very high bandwidth and reliability

Can vary; some are optimized for high interconnect (e.g., NVLink, InfiniBand)

Ecosystem & Integration

Tight integration with DevOps, databases, storage, analytics, security, identity

Lightweight—focused mainly on compute, with minimal frills

Flexibility

Broad platform: supports everything from web hosting to LLM training

Narrow focus: mainly training, inference, and fine-tuning workloads

Target Users

Large enterprises, governments, global-scale AI projects

Startups, researchers, model trainers, boutique AI labs

Innovation Cycle

Slower—must maintain enterprise stability

Faster—can pivot quickly to support new GPUs or AI frameworks

Example Use Case

Multi-cloud enterprise AI strategy integrating ERP + data lakes + model deployment

Cost-effective fine-tuning or inference serving for startups

How They’re Converging

There’s an emerging hybrid trend:

Hyperscalers are building specialized AI infrastructure (e.g., NVIDIA DGX Cloud partnerships, Microsoft–OpenAI collaboration, Google DeepMind integration).

Smaller AI compute providers are adding orchestration layers (e.g., API management, distributed training schedulers) to resemble mini hyperscalers.

Some mid-tier players like Oracle, IBM Cloud, and Tencent Cloud are positioning themselves between these two worlds — offering both enterprise reliability and AI specialization.

In Summary

Hyperscalers = scale, reliability, and enterprise integration; ideal for end-to-end AI systems.

AI Compute Clouds = agility, affordability, and specialization; ideal for developers or teams training and serving models directly.

Would you like me to include a comparison of cost-performance ratios for AI workloads (e.g., GPT model training on A100s vs TPUs vs custom silicon)? That can show where each platform has an advantage.

Some Emergent Hyperscalers

Nscale — a vertically-integrated AI data-centre / GPU cloud scale-play (rapidly expanding via large GPU supply deals and data-centre buildouts). nscale.com+1

CoreWeave — GPU-first cloud operator focused on ML/graphics workloads; positions itself as lower-cost, fast access to new NVIDIA hardware. CoreWeave

Lambda Labs (Lambda Cloud) — ML-first cloud and appliances for researchers and enterprises; early to H100/HGX and sells private clusters. lambda.ai

Vast.ai — a marketplace/aggregator that connects buyers to third-party GPU providers for low-cost, on-demand GPU rentals. Vast AI

RunPod — developer-friendly, pay-as-you-go GPU pods and serverless inference/fine-tuning; emphasizes per-second billing and broad GPU options. Runpod+1

Paperspace (Gradient / DigitalOcean partnership) — easy UX for ML workflows, managed notebook/cluster services; targets researchers and smaller teams. paperspace.com+1

FluidStack — builds and operates large GPU clusters / AI infrastructure for enterprises; touts low cost and large cluster deliveries (recent colocation/HPC deals). fluidstack.io+1

Nebius — full-stack AI cloud aiming at hyperscale enterprise contracts (recent large Microsoft capacity agreements and public listing activity). Nebius+1

Iris Energy (IREN) — originally a bitcoin miner now pivoting to GPU colocation / AI cloud (scaling GPU fleet and data-centre capacity). Data Center Dynamics+1

Comparison table

Provider

Business model

Typical hardware

Pricing model

Typical customers

Notable strength / recent news

Nscale

Build-own-operate AI data centres + sell GPU capacity

NVIDIA GB/B-class & other datacentre GPUs (mass GPU allocations)

Enterprise deals / reservations + cloud access

Large enterprises, cloud partners

Large GPU supply deals with Microsoft; fast expansion. nscale.com+1

Practical differences that matter when you pick one

Business model & reliability

Marketplace providers (Vast.ai) are great for cheap, experimental runs but carry variability in host reliability and support. Vast AI

Dedicated GPU clouds (CoreWeave, Lambda, FluidStack, Nebius, Nscale, Iris) provide more predictable SLAs and engineering support for production/federated training. nscale.com+4CoreWeave+4lambda.ai+4

Access to bleeding-edge hardware

Lambda and CoreWeave emphasize fast access to the newest NVIDIA stacks (H100, HGX/B200, etc.). Good if you need peak FLOPS. lambda.ai+1

Pricing predictability vs lowest cost

RunPod / Vast.ai / Paperspace often win on price for small / short jobs (per-second billing, spot marketplaces). For large, sustained runs, enterprise contracts with Nebius / Nscale / FluidStack or reserved capacity at Lambda/CoreWeave may be more cost-efficient. Runpod+2Vast AI+2

Scale & strategic partnerships

Nebius and Nscale are scaling via huge supply agreements and data-centre builds aimed at enterprise contracts (Microsoft news for both). That makes them candidates if you need tens of thousands of GPUs or long-term buying power. Reuters+1

Operational maturity & support

CoreWeave, Lambda, and Paperspace have mature dev experience / tooling and are used widely by ML teams. FluidStack and the miner pivots (Iris Energy) are moving fast into HPC/colocation and can offer very large capacity but may require more custom engagement. irisenergy.gcs-web.com+4CoreWeave+4lambda.ai+4

Experimentation / cheapest short runs: Vast.ai or RunPod. Vast AI+1

Research / fast access to newest GPUs: Lambda or CoreWeave. lambda.ai+1