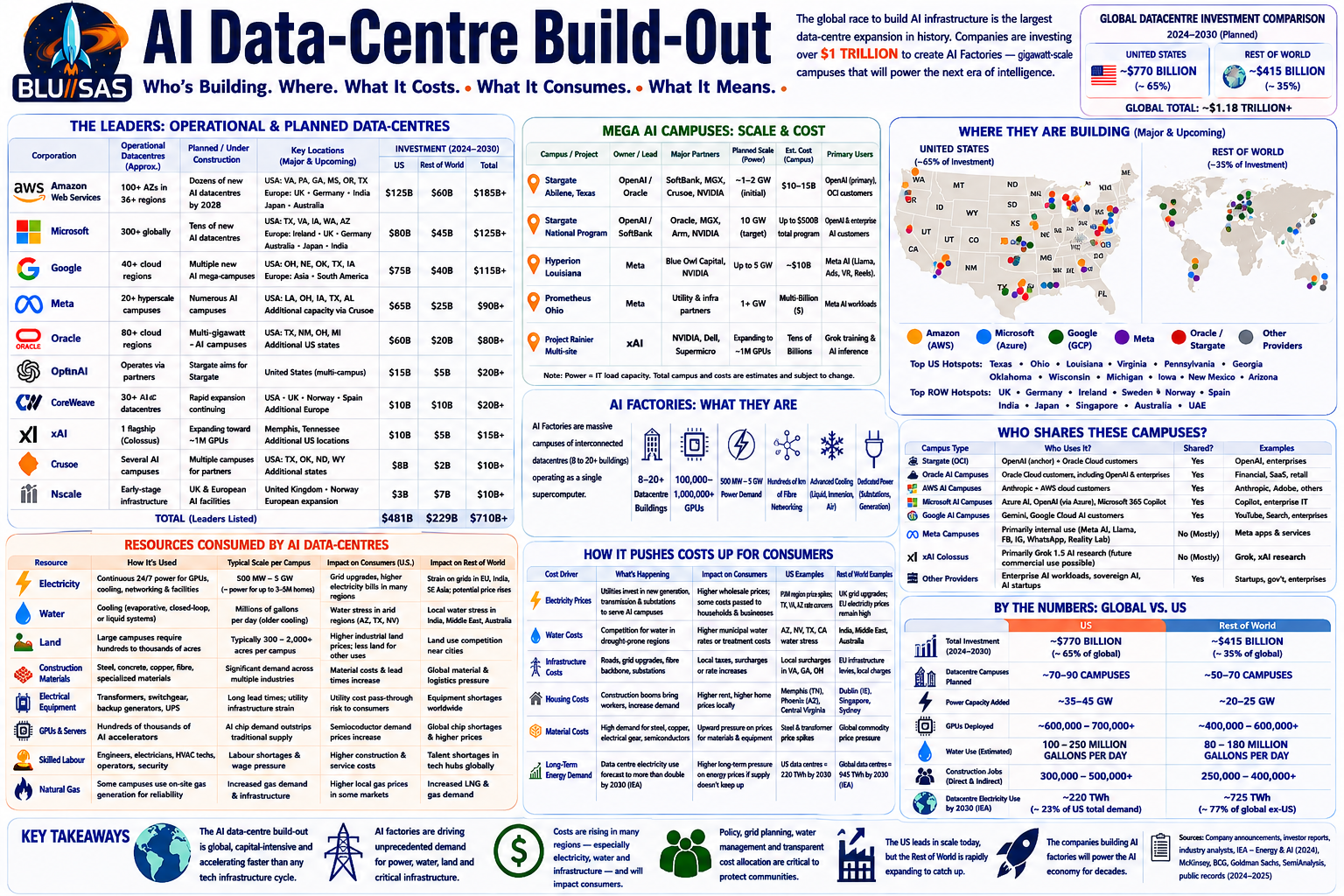

The AI infrastructure race is being led by a relatively small number of corporations, but together they represent well over US$1 trillion of planned investment over the remainder of this decade. Many figures below are approximate because companies often announce campuses or regions rather than exact building counts, and projects evolve rapidly.

| Corporation | Operational data centres (approx.) | AI data centres planned / under construction | Main locations |

|---|---|---|---|

| Amazon Web Services | 100+ availability zones across 36+ regions | Dozens of new AI campuses through 2028 (including Project Rainier) | USA (Virginia, Pennsylvania, Georgia, Mississippi, Oregon), Europe, UK, Germany, India, Japan, Australia |

| Microsoft | 300+ data centres globally | Tens of new AI campuses; ~$80B AI infrastructure investment | USA, Sweden, Finland, UK, Germany, Australia, Japan, Texas, Wisconsin |

| 40+ cloud regions and many hyperscale campuses | Multiple new AI mega-campuses | Ohio, Nebraska, Oklahoma, Texas, Iowa, Europe, Asia | |

| Meta | 20+ hyperscale campuses | Numerous AI campuses under expansion | Louisiana, Ohio, Iowa, Texas, Alabama, with additional capacity from Crusoe |

| Oracle | 80+ cloud regions | Multi-gigawatt AI campuses via Stargate plus Oracle Cloud expansion | Texas, New Mexico, Ohio, Michigan and other US states |

| OpenAI | Operates via partners rather than owning a global DC fleet | Stargate aims for roughly 20 major AI campuses | Texas, New Mexico, Ohio, Wisconsin, Michigan and additional US sites |

| SoftBank | No major hyperscale cloud estate | Co-investor in Stargate | United States (multiple campuses) |

| CoreWeave | ~30+ AI data centres | Continuing rapid expansion | USA, UK, Norway, Spain and additional European sites |

| xAI | 1 flagship AI supercluster (Colossus) plus expansions | Expanding toward one million GPUs | Memphis, Tennessee and additional US locations |

| Crusoe | Several AI campuses under operation | Multiple campuses for OpenAI, Meta and Microsoft | Texas, Oklahoma and other US states |

| Nscale | Early-stage AI infrastructure | UK and European sovereign AI facilities planned | United Kingdom, Norway and Europe (build-out still in early stages) |

Where the biggest build-out is happening

The current hotspots are:

- Texas – by far the largest concentration, with Stargate, Oracle, Microsoft, Google and xAI all investing heavily.

- Ohio – Google, Meta and Oracle are all expanding there.

- Louisiana – Meta’s enormous AI campus.

- Virginia – still the world’s largest concentration of conventional cloud data centres.

- Pennsylvania, Georgia and Oklahoma – major AWS and Google investments.

- Wisconsin, Michigan and New Mexico – emerging AI infrastructure hubs.

The scale is unprecedented

The six largest AI infrastructure builders (Amazon, Microsoft, Google, Meta, Oracle and the Stargate consortium) have collectively committed around US$690–700 billion in AI-related capital expenditure, with 74 new AI-focused projects breaking ground in the US during 2026 alone. Longer-term projections suggest total AI infrastructure investment could exceed US$5 trillion globally by 2030.

One notable trend is that these companies are no longer building isolated data centres. They are constructing AI campuses consisting of anywhere from 8 to more than 20 individual data-centre buildings, all linked by ultra-high-speed networking so they function as a single giant AI supercomputer. A single campus can consume 500 MW to over 1 GW of power, equivalent to the electricity demand of a medium-sized city.

The largest AI campuses consume enormous quantities of resources. Some impacts are already measurable, while others remain uncertain and depend on how utilities allocate costs. It’s important to distinguish local effects (which can be substantial) from national effects (which are often much smaller).

| Resource | How AI campuses use it | Impact on consumers |

|---|---|---|

| Electricity | Hundreds of MW to several GW continuously | Higher utility investment, possible higher electricity bills in constrained regions, increased need for new power stations |

| Water | Cooling systems can consume millions of gallons per day, although newer designs increasingly use closed-loop or air cooling | Competition for water in drought-prone areas; pressure on municipal supplies |

| Land | Campuses often occupy hundreds to thousands of acres | Industrial land values rise; reduced land available for other development |

| Construction materials | Steel, concrete, copper, fibre-optic cable | Higher demand can contribute to material price increases, though AI is only one of several drivers |

| Electrical equipment | Transformers, switchgear, substations | Longer lead times for utilities and industrial customers |

| GPUs and servers | Hundreds of thousands of accelerators per campus | Semiconductor manufacturing capacity diverted toward AI, increasing demand for advanced chips |

| Skilled labour | Electrical engineers, construction workers, data-centre technicians | Wage competition and labour shortages in some regions |

| Natural gas | Some campuses are building dedicated gas-fired generation | Increased demand for gas infrastructure and fuel in certain markets |

Electricity prices

Electricity is the area where households are most likely to notice an effect.

Large AI campuses require utilities to invest in:

- New transmission lines

- New substations

- Additional generation

- Grid upgrades

Who pays depends on regulation.

In some regions, regulators are trying to ensure that AI companies pay most of these costs. In others, some infrastructure costs are spread across all customers, which can increase household bills.

For example:

| Region | Reported effect |

|---|---|

| PJM (eastern U.S.) | Wholesale electricity prices rose sharply as demand from AI data centres increased, prompting calls for tech companies to fund more of the required infrastructure. |

| Arizona | Utilities warn that electricity infrastructure may need to roughly double within a few years because of AI growth. |

| Virginia | Data centres already account for a very large share of electricity demand in some parts of the state. |

It’s also worth noting that recent academic work found that, historically (2015–2024), data centres slightly reduced average U.S. electricity prices by helping spread fixed grid costs over more customers. The authors caution that this may not hold if future supply constraints become severe.

Water

Water is highly location-dependent.

Older evaporative cooling systems can use several million gallons of water per day. Newer AI facilities increasingly employ:

- Closed-loop liquid cooling

- Direct-to-chip liquid cooling

- Air cooling where practical

These approaches can significantly reduce freshwater consumption, but water remains a concern in arid regions.

Housing

AI campuses can affect local housing markets by:

- Bringing thousands of construction workers

- Creating highly paid engineering jobs

- Increasing demand for rental accommodation

The effect is usually local rather than national.

Employment

Benefits include:

- Construction employment

- Electrical contracting

- Operations and maintenance jobs

- Security

- Network engineering

- Mechanical engineering

However, once operational, AI campuses employ far fewer people than factories of similar size.

Have prices increased?

Evidence is mixed:

| Item | Observed trend |

|---|---|

| Electricity | Some U.S. regions have seen higher wholesale prices and concerns about retail bills where AI demand is concentrated. |

| Water | Mostly local impacts in water-stressed regions rather than broad consumer price rises. |

| Housing | Local increases around major developments are common, though driven by multiple factors. |

| Construction materials | Increased demand contributes to pressure, but AI is only one of many drivers. |

| Consumer goods | There is currently little evidence that AI data centres have directly increased the prices of everyday retail goods. |

Overall, the greatest measurable impact today is on electricity infrastructure. The International Energy Agency projects that global data-centre electricity consumption will more than double to about 945 TWh by 2030, driven largely by AI. Whether households ultimately pay more depends on regulatory decisions about who funds the new power plants, transmission lines and substations needed to support these AI campuses.

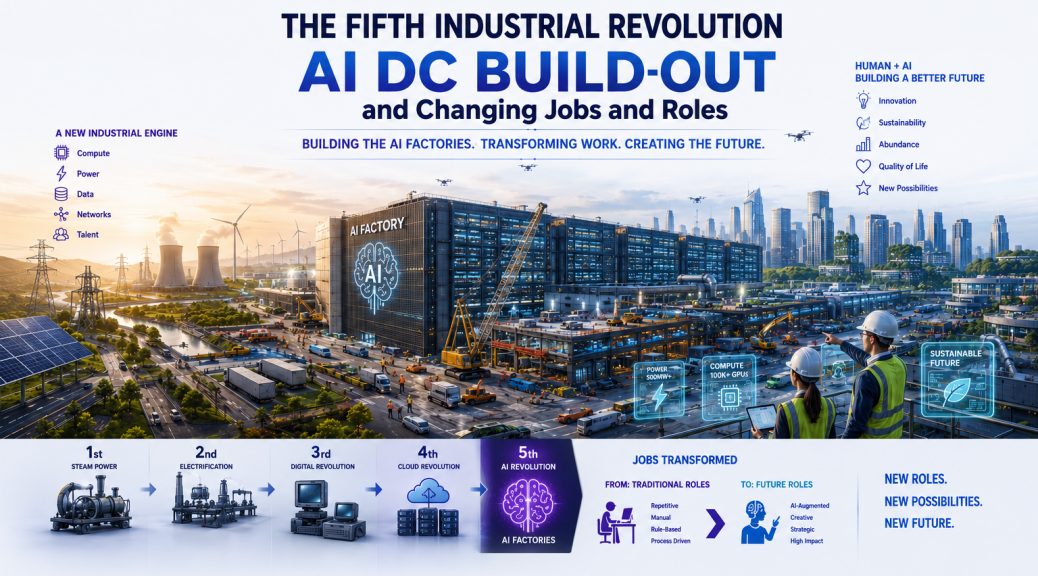

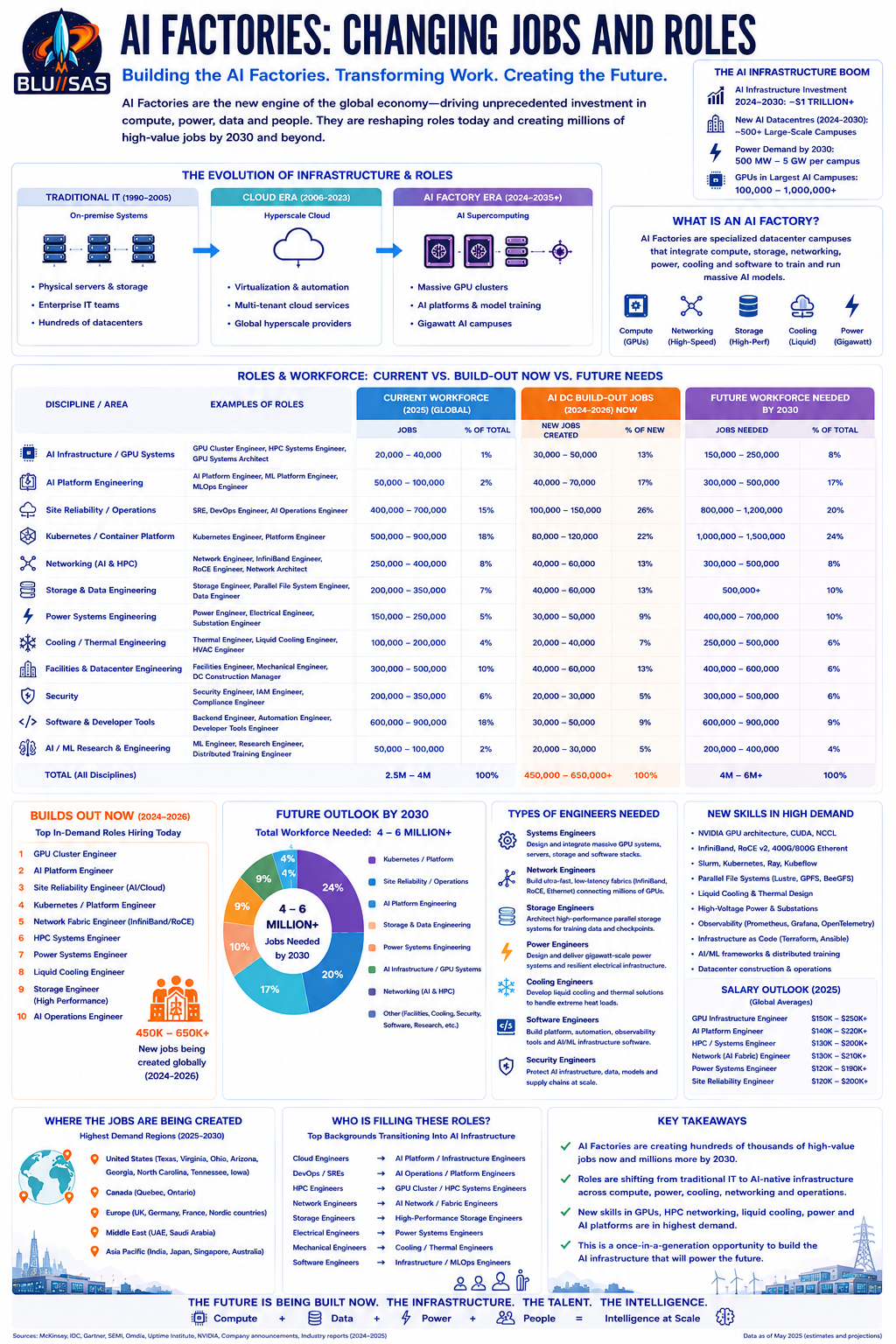

Changing Jobs and Roles

The AI infrastructure boom is creating the largest shift in infrastructure engineering since the rise of public cloud around 2006–2015. Traditional cloud providers needed engineers to build reliable, scalable services for virtual machines, storage and networking. AI Factories require all of that plus expertise in GPUs, ultra-high-speed networking, power engineering, liquid cooling and AI software platforms.

Evolution of Infrastructure Engineering

| Era | Primary Goal | Main Infrastructure | Typical Employer |

|---|---|---|---|

| Enterprise IT (1990–2010) | Business applications | Servers, SAN, LAN | Banks, government, enterprises |

| Cloud (2006–2024) | Multi-tenant cloud services | Hyperscale datacenters | AWS, Azure, Google Cloud |

| AI Factory (2024–2035+) | Massive AI computation | GPU supercomputers, AI campuses | OpenAI, Meta, xAI, Oracle, CoreWeave, Nscale, AWS |

Traditional Cloud Provider Jobs

Cloud providers traditionally organised engineering into around a dozen major disciplines.

| Discipline | Typical Roles |

|---|---|

| Datacenter Facilities | Facilities Engineer, Mechanical Engineer, Electrical Engineer |

| Compute | Server Engineer, Linux Engineer, Virtualisation Engineer |

| Storage | Storage Engineer, Ceph Engineer, SAN Engineer |

| Networking | Network Engineer, Network Architect |

| Cloud Platform | Kubernetes Engineer, OpenStack Engineer, VMware Engineer |

| Reliability | Site Reliability Engineer (SRE), DevOps Engineer |

| Security | Security Engineer, IAM Engineer |

| Observability | Monitoring Engineer, Logging Engineer |

| Automation | Ansible Engineer, Terraform Engineer |

| Software | Backend Engineer, Platform Engineer |

| Operations | NOC Engineer, Incident Manager |

| Capacity | Capacity Planner, Performance Engineer |

A large hyperscale datacenter typically employs 100–300 permanent staff, with many more contractors during construction.

AI Factory Engineering

AI Factories introduce entirely new engineering domains.

| New Discipline | Example Roles |

|---|---|

| GPU Infrastructure | GPU Systems Engineer, GPU Cluster Engineer |

| AI Networking | InfiniBand Engineer, RoCE Engineer, Ethernet Fabric Engineer |

| AI Storage | High-performance Storage Engineer, Parallel Filesystem Engineer |

| AI Cooling | Liquid Cooling Engineer, Thermal Systems Engineer |

| AI Scheduling | Slurm Engineer, Kubernetes AI Platform Engineer |

| AI Runtime | CUDA Engineer, Distributed Training Engineer |

| AI Optimisation | ML Infrastructure Engineer |

| AI Datacenter Power | High-voltage Power Engineer |

| AI Chip Engineering | Accelerator Integration Engineer |

| AI Operations | AI Infrastructure SRE |

Engineering Stack

Traditional cloud:

Applications

Containers

Virtual Machines

Hypervisor

Servers

Storage

Networking

PowerAI Factory:

AI Models

Distributed Training

Kubernetes / Slurm

CUDA / ROCm

100,000+ GPUs

InfiniBand / RoCE

Parallel Storage

Liquid Cooling

Gigawatt PowerTraditional Cloud Skills

- Linux

- VMware

- Kubernetes

- OpenStack

- AWS

- Azure

- Terraform

- Ansible

- Prometheus

- Grafana

- Python

- Go

- Storage

- Networking

New AI Factory Skills

Additional skills now becoming highly valuable include:

- NVIDIA GPU architecture

- AMD Instinct

- CUDA

- NCCL

- GPUDirect RDMA

- InfiniBand

- RoCE v2

- Slurm

- Ray

- Kubeflow

- MLFlow

- Triton Inference Server

- Parallel file systems (Lustre, IBM Storage Scale/GPFS, BeeGFS)

- High-performance Ethernet (400/800 GbE)

- Direct-to-chip liquid cooling

- Rack-scale power engineering

Jobs Growing Fastest

| Role | Growth Outlook |

|---|---|

| GPU Infrastructure Engineer | Extremely High |

| AI Platform Engineer | Extremely High |

| HPC Systems Engineer | Extremely High |

| Kubernetes Platform Engineer | Very High |

| Storage Engineer | Very High |

| Site Reliability Engineer | Very High |

| Network Fabric Engineer | Extremely High |

| Power Systems Engineer | Extremely High |

| Mechanical Cooling Engineer | Extremely High |

| AI Operations Engineer | Extremely High |

Approximate Current Workforce (2025–2026)

The exact numbers are difficult to measure because many roles overlap, but industry estimates suggest:

| Profession | Estimated Global Workforce |

|---|---|

| Cloud Engineers | 2–3 million |

| DevOps Engineers | 1.5–2 million |

| Site Reliability Engineers | 400,000–700,000 |

| Kubernetes Engineers | 500,000–900,000 |

| Datacenter Engineers | 300,000–500,000 |

| Storage Engineers | 200,000–350,000 |

| HPC Engineers | 80,000–150,000 |

| GPU Infrastructure Specialists | 20,000–40,000 |

| AI Infrastructure Engineers | 50,000–100,000 |

Estimated Workforce Needed by 2030

As AI campuses proliferate worldwide, demand is expected to increase significantly.

| Profession | Estimated Demand by 2030 |

|---|---|

| AI Infrastructure Engineers | 300,000–500,000 |

| GPU Cluster Engineers | 150,000–250,000 |

| HPC Engineers | 250,000–400,000 |

| SREs (AI/Cloud) | 800,000–1.2 million |

| Kubernetes Platform Engineers | 1–1.5 million |

| Network Fabric Engineers | 300,000–500,000 |

| Storage Engineers | 500,000+ |

| Power Engineers | 400,000–700,000 |

| Cooling Engineers | 250,000–500,000 |

These are indicative estimates derived from announced AI infrastructure expansion plans and broader industry workforce analyses rather than official forecasts.

Where the Talent Is Coming From

Most AI Factory engineers are not newly trained graduates. Companies are recruiting experienced professionals from adjacent disciplines:

| Previous Role | Transition To |

|---|---|

| Cloud Engineer | AI Platform Engineer |

| Kubernetes Engineer | AI Infrastructure Engineer |

| SRE | AI Operations Engineer |

| HPC Engineer | GPU Cluster Engineer |

| Linux Engineer | GPU Systems Engineer |

| Network Engineer | InfiniBand/RoCE Fabric Engineer |

| Storage Engineer | AI Storage Architect |

| OpenStack Engineer | AI Cloud Platform Engineer |

| Ceph Engineer | High-performance Storage Engineer |

| DevOps Engineer | ML Platform Engineer |

Why This Matters

The next decade is likely to see a shift similar to the transition from enterprise IT to cloud computing. During the 2010s, the most sought-after roles were Cloud Engineers, DevOps Engineers and SREs. Through the late 2020s and into the 2030s, many of the highest-demand infrastructure roles are expected to centre on AI Factories: designing, building and operating gigawatt-scale GPU campuses, high-performance storage systems, ultra-low-latency networks and AI platforms.

For someone with expertise in Linux, Kubernetes, observability, automation, storage and cloud infrastructure, the progression into AI infrastructure engineering is relatively direct. Adding knowledge of GPU platforms, HPC networking (InfiniBand/RoCE), parallel storage (such as Lustre or GPFS), Slurm, CUDA and liquid-cooled datacenter design positions engineers for many of the roles expected to see the strongest demand over the coming decade.

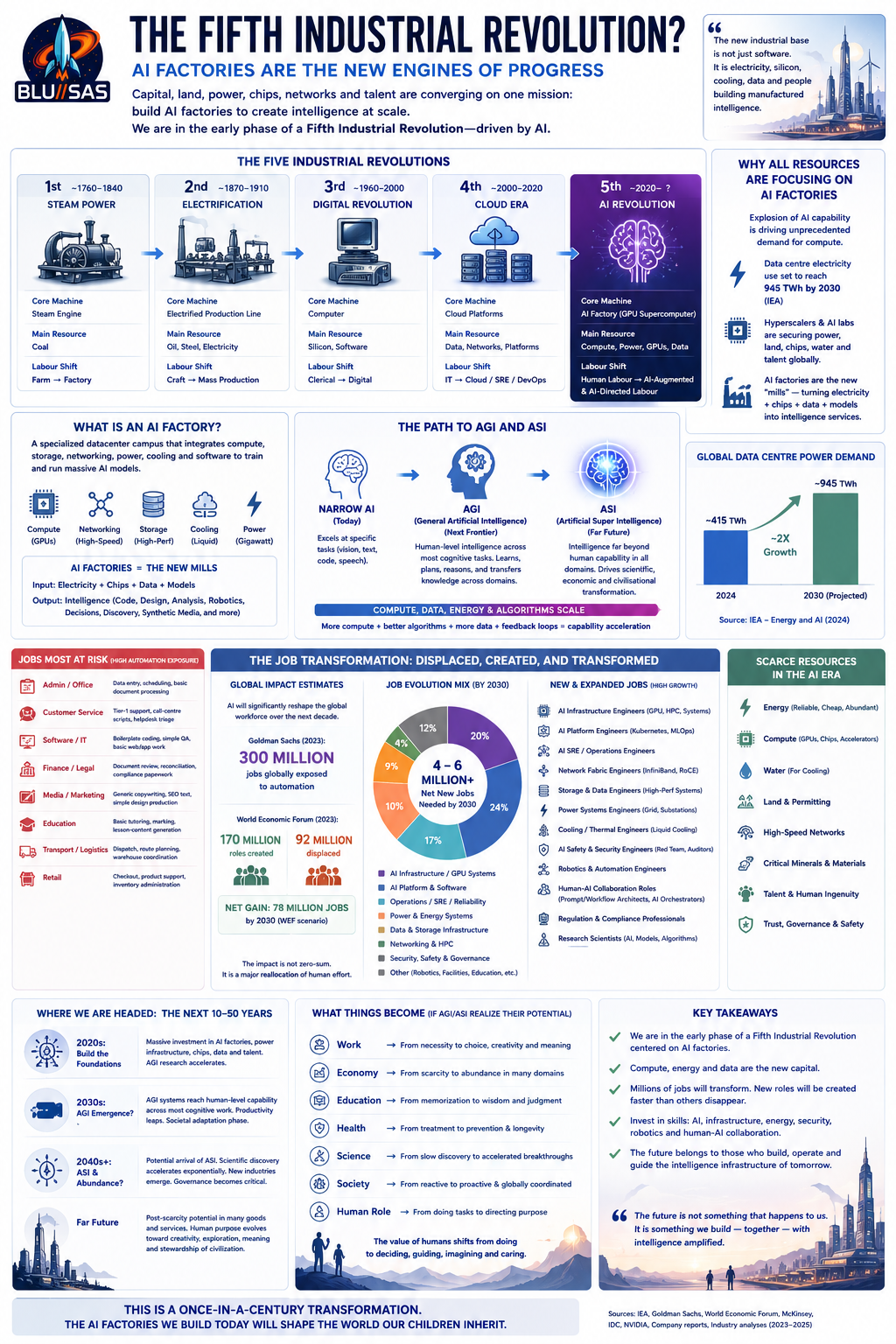

The Fifth Industrial Revolution?

Yes — this is plausibly the early phase of a Fifth Industrial Revolution, but with one caveat: we do not yet know whether AGI/ASI will arrive, or when. What is clear is that capital, land, power, water, chips, networks and engineering labour are being redirected toward AI factories.

The simplest framing:

| Industrial phase | Core machine | Main resource | Main labour shift |

|---|---|---|---|

| 1st | Steam engine | Coal | Farm → factory |

| 2nd | Electrified production line | Oil, steel, electricity | Craft → mass production |

| 3rd | Computer | Silicon, software | Clerical → digital |

| 4th | Cloud + automation | Data, networks, platforms | IT → cloud/SRE/DevOps |

| 5th | AI factory | Compute, power, GPUs, data | Human labour → AI-augmented/AI-directed labour |

The AI factory is the new “mill.” Instead of spinning cotton or stamping cars, it converts electricity + chips + data + models into intelligence services: code, design, analysis, customer support, robotics control, synthetic media, drug discovery and eventually autonomous decision systems.

The resource pull is already visible. The IEA projects global data-centre electricity consumption could roughly double to about 945 TWh by 2030, growing far faster than general electricity demand. That is why hyperscalers, AI labs and neoclouds are racing to secure power, grid connections, GPUs, cooling, land and engineering staff.

On jobs, the likely pattern is not “all jobs disappear.” It is task compression: fewer people needed for routine cognitive work, more people needed for infrastructure, supervision, security, robotics, energy, regulation and high-complexity design. Goldman Sachs has estimated that AI could expose the equivalent of 300 million full-time jobs globally to automation, while the World Economic Forum projects by 2030 about 170 million roles created and 92 million displaced, for a net gain of 78 million under its surveyed-employer scenario.

Likely traditional jobs under pressure:

| Area | Jobs most exposed |

|---|---|

| Admin/office | Data entry, scheduling, basic document processing |

| Customer service | Tier-1 support, call-centre scripts, helpdesk triage |

| Software | Boilerplate coding, simple QA, basic web/app work |

| Finance/legal | Document review, reconciliation, compliance paperwork |

| Media/marketing | Generic copywriting, SEO text, simple design production |

| Education | Basic tutoring, marking, lesson-content generation |

| Transport/logistics | Dispatch, route planning, warehouse coordination |

| Retail | Checkout, product support, inventory admin |

New and expanded jobs:

| Future area | Roles likely to grow |

|---|---|

| AI infrastructure | GPU cluster engineer, AI SRE, AI platform engineer |

| Power/grid | Substation engineer, energy systems engineer, microgrid operator |

| Cooling/facilities | Liquid-cooling engineer, thermal engineer, datacenter mechanic |

| Networking | InfiniBand/RoCE engineer, optical network engineer |

| Storage/data | Parallel storage engineer, data governance engineer |

| AI safety/security | Model auditor, AI red-team engineer, AI incident responder |

| Robotics | Robot fleet supervisor, autonomy technician, human-robot workflow designer |

| Regulation | AI compliance officer, algorithmic accountability auditor |

| Human-AI work | Agent orchestrator, prompt/workflow architect, AI operations manager |

| Synthetic worlds | Simulation designer, digital twin engineer, synthetic-data engineer |

If AGI arrives, the shift accelerates. If ASI arrives, the shift becomes civilisational: the scarce resources may become energy, compute rights, physical materials, robotics capacity, trusted governance and human legitimacy, rather than ordinary labour.

So yes: the AI build-out looks like the physical foundation of a Fifth Industrial Revolution — not just software, but a new industrial base built around manufactured intelligence.