“Neocloud” (sometimes written neo cloud) is a term for a new generation of cloud providers that specialize in AI computing rather than offering the full range of traditional cloud services. They focus heavily on providing high-performance GPUs for AI training and inference.

How neoclouds differ from traditional cloud providers

| Traditional cloud (AWS, Azure, Google Cloud) | Neocloud |

|---|---|

| Broad range of services (databases, storage, networking, analytics, etc.) | Primarily focused on AI and GPU computing |

| Designed for many types of workloads | Optimized specifically for AI/ML workloads |

| Large hyperscale platforms | Often smaller, AI-focused companies |

| GPU capacity can be limited or expensive | Aim to provide faster access to GPUs and lower costs |

Why neoclouds became popular

The explosion of generative AI created huge demand for GPUs such as NVIDIA H100 and Blackwell chips. Many organizations struggled to obtain enough AI compute from traditional cloud providers, creating an opportunity for specialized GPU cloud companies.

Examples of neocloud providers

Some well-known neocloud companies include:

- CoreWeave

- Lambda

- Crusoe

- Nebius

- Together AI

These companies provide GPU-as-a-Service (GPUaaS) and AI-focused infrastructure.

Simple analogy

Think of traditional cloud providers as a large supermarket that sells everything, while a neocloud is a specialty store focused almost entirely on AI computing power. It may offer fewer services overall, but it is optimized for AI workloads and often provides better access to GPUs.

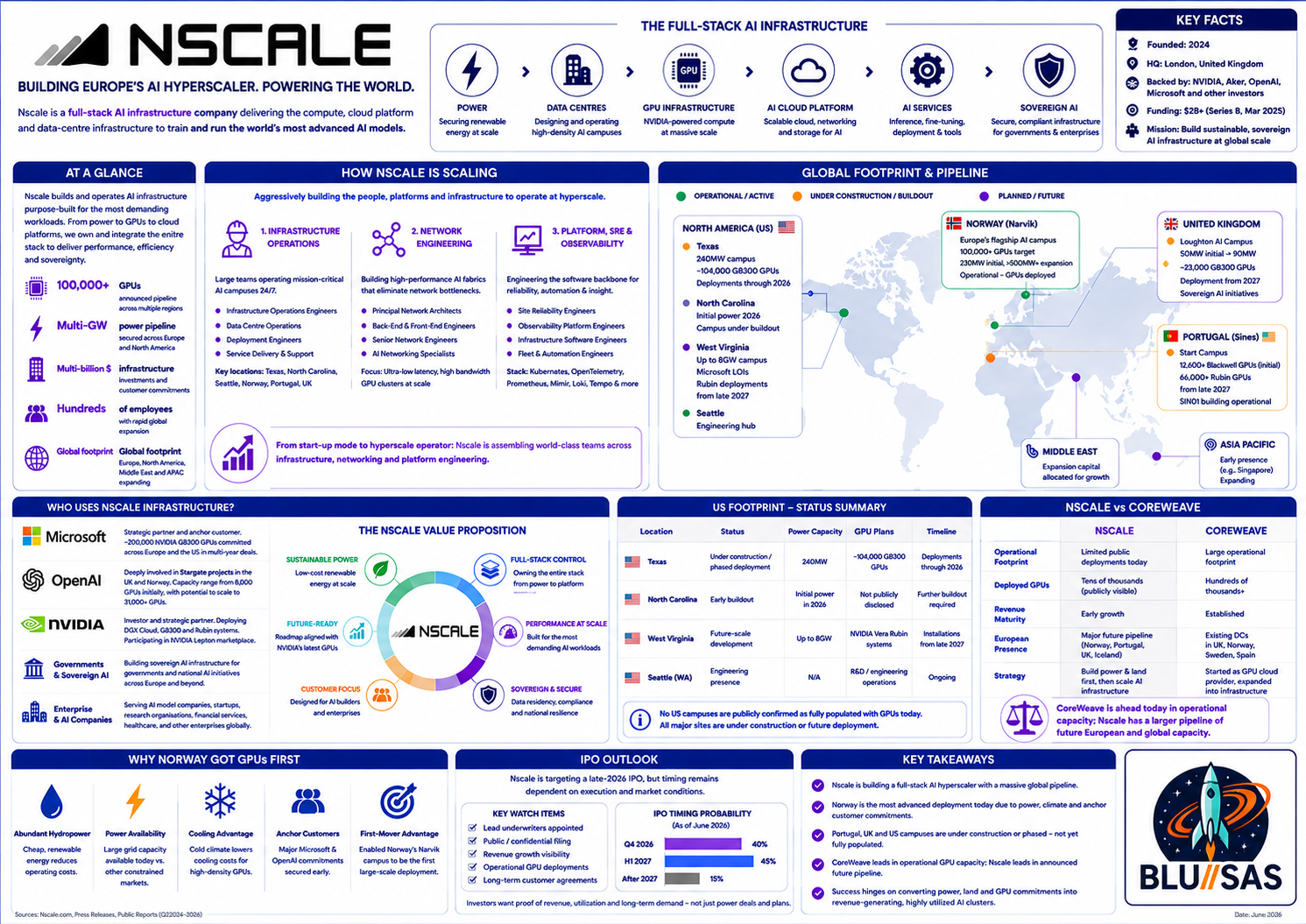

Nscale a European Neocloud?

Today, a more representative list of major neoclouds would include:

| Company | Region | Notes |

|---|---|---|

| Nscale | UK / Europe | Full-stack AI infrastructure, sovereign AI cloud, GPU cloud, data centre developer. |

| CoreWeave | US | Often regarded as the archetypal neocloud. |

| Nebius | Europe | AI cloud and GPU infrastructure provider. |

| Lambda | US | GPU cloud focused on AI training and inference. |

| Crusoe | US | AI data centres and GPU cloud infrastructure. |

| Together AI | US | AI platform plus infrastructure. |

Nscale’s positioning is actually slightly different from some of the others because it is trying to be vertically integrated:

- Building or owning AI data centres.

- Procuring GPU fleets at massive scale.

- Operating AI cloud services.

- Offering sovereign AI infrastructure for governments and enterprises.

- Running full-stack AI platforms rather than just renting GPUs.

Some analysts now classify Nscale as an AI hyperscaler rather than merely a neocloud because of the scale it is targeting. ABI Research ranked Nscale as the overall leader among 14 neocloud providers in its 2026 assessment.

What’s interesting is that the neocloud landscape appears to be splitting into three tiers:

- GPU rental companies – essentially GPU-as-a-Service.

- AI cloud platforms – GPUs plus AI tooling.

- AI hyperscalers – own data centres, networking, power, GPUs, and cloud platform.

Nscale is deliberately pursuing category 3. The company describes itself as a vertically integrated AI cloud and has announced very large-scale deployments in Europe and the US.

If you compare Nscale, CoreWeave, and Crusoe specifically, I’d place them like this:

| Area | Nscale | CoreWeave | Crusoe |

|---|---|---|---|

| Sovereign European AI | Strongest | Limited | Limited |

| GPU Cloud | Strong | Very Strong | Strong |

| Data Centre Ownership | Extensive strategy | Growing | Extensive |

| AI Hyperscaler Ambition | Very High | High | High |

| European Presence | Strongest | Moderate | Moderate |

| Microsoft Partnerships | Significant | Significant | Significant |

From a European perspective, Nscale is probably the closest thing Europe currently has to a home-grown AI hyperscaler.

No. If we’re talking about Europe specifically, I would actually argue the opposite:

CoreWeave is currently ahead in deployed AI infrastructure, while Nscale is ahead in announced future European capacity.

Those are very different things.

CoreWeave’s position in Europe

CoreWeave already has:

- European headquarters in London.

- Two operational UK data centres.

- Expansion into Norway, Sweden, and Spain.

- Billions already committed and deployed into European infrastructure.

- A mature GPU cloud platform that is already serving customers globally.

By 2025, CoreWeave had announced European expansion into Norway, Sweden, and Spain alongside its existing UK footprint.

More importantly, CoreWeave entered Europe after already becoming a large-scale AI cloud provider in the US. They brought:

- Operational expertise

- Existing customers

- Existing software platform

- Existing GPU fleet

That is a major advantage.

Where Nscale is stronger

Nscale’s strength is the future build pipeline.

Publicly announced projects include:

- Stargate Norway

- Sines (Portugal)

- UK AI campus developments

- Iceland expansion plans

Some of these projects are absolutely enormous on paper. The Norway Stargate project alone targets 100,000 NVIDIA GPUs.

Portugal is also positioned as one of Nscale’s flagship European hubs, with 12,600+ Blackwell GPUs initially and much larger Rubin deployments planned later.

The key distinction

If you compare today’s operational reality:

| Metric | CoreWeave | Nscale |

|---|---|---|

| Operational GPU cloud | Ahead | Behind |

| Existing customer workloads | Ahead | Behind |

| Software/cloud platform maturity | Ahead | Behind |

| European operational experience | Ahead | Behind |

| Publicly visible deployed GPU capacity | Ahead | Behind |

If you compare future announced European capacity:

| Metric | CoreWeave | Nscale |

|---|---|---|

| Norway buildout | Large | Very large |

| Portugal | Limited public presence | Major flagship site |

| Sovereign AI initiatives | Some | Strong focus |

| OpenAI-linked projects | Limited | Significant |

| Future European MW pipeline | Large | Potentially larger |

A useful analogy

Today, CoreWeave is closer to:

“We already run a large AI cloud and are expanding into Europe.”

Nscale is closer to:

“We are building some of Europe’s largest AI campuses and will become a major AI cloud.”

Those are different stages of maturity.

The question investors are asking

The debate isn’t really:

“Can Nscale catch CoreWeave?”

The debate is:

“Can Nscale turn announced power, land, and GPU commitments into revenue-producing clusters before demand or financing conditions change?”

CoreWeave has already demonstrated it can operate large GPU fleets and monetize them. Nscale is in the process of proving that at the same scale.

One interesting point: some recent reporting has questioned the extent to which both companies’ European investment announcements translate into immediately operational facilities, noting that some “new data centre” claims are actually deployments into existing colocation facilities rather than brand-new campuses. That criticism has been directed at both Nscale and CoreWeave.

So as of mid-2026:

- Operationally: CoreWeave is ahead in Europe.

- Announced future European capacity: Nscale may have the larger headline pipeline.

- Execution risk: Nscale has more to prove because a larger proportion of its European footprint is still future-dated.

Is Nscale’s IPO still on target for late 2026?

As of June 2026, there is no publicly filed prospectus, no announced exchange, and no confirmed IPO date for Nscale.

The strongest public indication that an IPO is still being pursued comes from industry reports stating that Nscale was planning a fall/late-2026 IPO and was pursuing additional US data-centre acquisitions ahead of that listing.

However, there are several reasons to be cautious about assuming it is “on target”:

Reasons it could still happen in late 2026

- The AI infrastructure sector remains one of the hottest areas in public markets.

- Investors have rewarded AI infrastructure companies such as CoreWeave since its public debut.

- Nscale has announced very large infrastructure commitments involving Microsoft and multiple multi-hundred-megawatt campuses, which is the type of growth story public investors currently like.

Reasons it could slip into 2027

The challenge is that public-market investors increasingly want proof of:

- Revenue growth

- Actual GPU deployments

- Utilization rates

- Long-term customer contracts

- Cash-flow visibility

rather than just power agreements and future construction plans.

Unlike CoreWeave, which entered public markets after operating large GPU fleets for years, much of Nscale’s most ambitious capacity remains future-dated. That creates execution risk that investors will scrutinize heavily.

What I would watch for

If Nscale is genuinely targeting a late-2026 IPO, I would expect to see during the next few months:

- Appointment of lead underwriters (Goldman Sachs, Morgan Stanley, JPMorgan, etc.).

- Public filing activity or confidential filing reports.

- More detailed revenue disclosures.

- Announcements of operational GPU deployments, not just planned deployments.

- Additional long-term customer agreements.

My assessment

If I had to assign probabilities today:

| Outcome | Probability |

|---|---|

| IPO in Q4 2026 | ~40% |

| IPO slips into H1 2027 | ~45% |

| IPO delayed beyond 2027 | ~15% |

That’s not based on any insider information—just on where Nscale appears to be in its infrastructure rollout compared with where most AI infrastructure companies are when they ring the bell.

The most important signal is not the IPO date itself. It’s whether Nscale can demonstrate that its Norway, Texas, Portugal, and future UK capacity are being converted into revenue-generating GPU clusters with high utilization. If that evidence emerges during 2026, a late-2026 IPO becomes much more plausible.

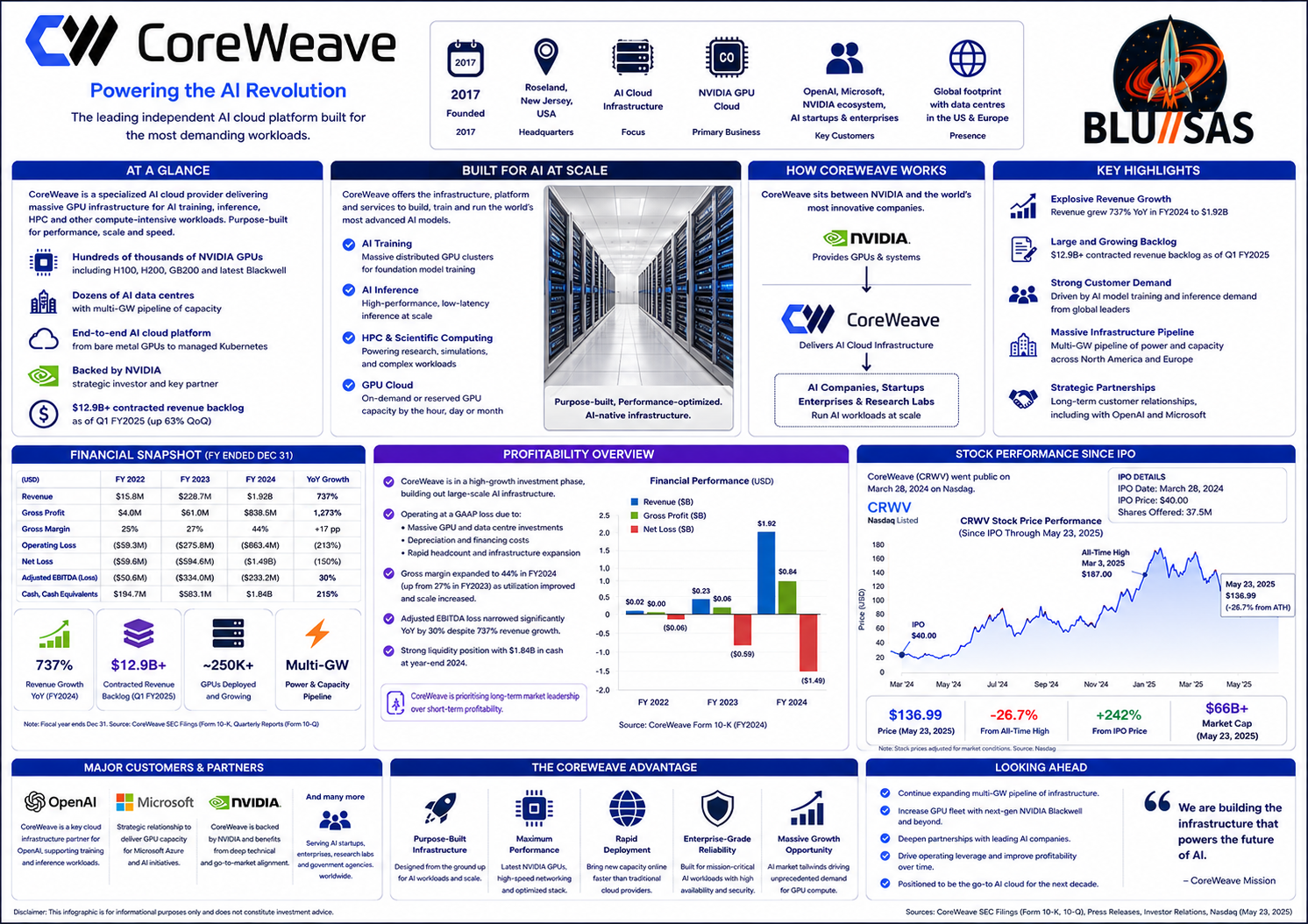

CoreWeave

CoreWeave is an AI cloud provider that specializes in delivering large-scale GPU infrastructure for AI training, inference, HPC, rendering, and scientific computing.

The company started life as a GPU-focused cloud provider and has evolved into one of the largest independent AI infrastructure companies in the world.

Unlike AWS, Azure, and Google Cloud, which offer AI as part of a broader cloud portfolio, CoreWeave is almost entirely focused on GPU-accelerated workloads.

| Category | Details |

|---|---|

| Founded | 2017 |

| Headquarters | Roseland, New Jersey, USA |

| Focus | AI Cloud Infrastructure |

| Primary Business | GPU-as-a-Service |

| Main Customers | OpenAI, Microsoft, NVIDIA ecosystem, AI startups |

| Major Hardware | NVIDIA H100, H200, GB200, Blackwell |

| Competitors | AWS, Azure, Google Cloud, Crusoe, Lambda, Nscale |

How CoreWeave Started

The company originally operated in cryptocurrency mining.

Management realized early that:

- GPUs used for mining

- GPUs used for AI training

- GPUs used for rendering

all required similar infrastructure.

When the AI boom began following the success of ChatGPT, CoreWeave pivoted aggressively into AI compute.

This turned out to be one of the best-timed pivots in the technology industry.

CoreWeave’s Business Model

Think of CoreWeave as:

NVIDIA

↓

CoreWeave

↓

AI CompaniesInstead of:

NVIDIA

↓

Microsoft Azure

AWS

Google Cloud

↓

AI CompaniesCoreWeave sits between NVIDIA and AI customers.

What Services Does CoreWeave Offer?

1. AI Training Clusters

Used for:

- Large Language Models (LLMs)

- Foundation Models

- Multimodal Models

- Scientific AI

Examples:

- GPT-style models

- Image generation models

- Robotics models

Typical infrastructure:

- Thousands of GPUs

- InfiniBand networking

- Petabytes of storage

2. AI Inference

After a model is trained:

Training

↓

Model

↓

InferenceInference is what happens when:

- You ask ChatGPT a question

- Generate an image

- Run a chatbot

CoreWeave provides infrastructure for this at scale.

3. HPC

High Performance Computing workloads:

- Weather modelling

- Genomics

- Drug discovery

- CFD

- Physics simulations

This is an area where CoreWeave competes with traditional HPC centres.

4. GPU Cloud

Instead of buying:

- H100s

- H200s

- Blackwell systems

Customers rent them by:

- Hour

- Day

- Month

Why NVIDIA Likes CoreWeave

NVIDIA has invested in CoreWeave because CoreWeave helps NVIDIA:

- Deploy GPUs faster

- Reach AI startups

- Increase GPU utilization

- Expand GPU cloud capacity

NVIDIA has been both a supplier and investor.

CoreWeave Infrastructure

Typical CoreWeave clusters contain:

NVIDIA GPUs

│

InfiniBand

│

GPU Nodes

│

High-speed Storage

│

Kubernetes

│

Customer WorkloadsTechnologies typically include:

- NVIDIA DGX

- HGX

- InfiniBand

- RoCE

- Kubernetes

- Slurm

- Object Storage

How Big is CoreWeave?

By 2026, CoreWeave is operating or building infrastructure measured in:

- Hundreds of thousands of GPUs

- Multiple gigawatts of power

- Dozens of AI data centres

This puts them among the largest AI-focused cloud providers globally.

Why Microsoft Matters

One of CoreWeave’s biggest customers has been Microsoft.

Microsoft has used CoreWeave capacity to supplement Azure AI infrastructure when Azure could not provision GPUs quickly enough.

This relationship helped accelerate CoreWeave’s growth enormously.

CoreWeave vs Nscale

| Area | CoreWeave | Nscale |

|---|---|---|

| Founded | 2017 | 2024 |

| Stage | Mature AI cloud | Emerging AI hyperscaler |

| GPUs Deployed Today | Very Large | More Limited |

| Revenue | Much Higher | Earlier Growth |

| Operational Experience | Extensive | Building |

| US Presence | Major | Growing |

| Europe Presence | Growing | Large Future Pipeline |

| Data Centres | Operating Today | Many Future Builds |

| AI Cloud Platform | Mature | Developing |

What Would Interest an SRE?

For someone coming from:

- Kubernetes

- Observability

- OpenTelemetry

- Prometheus

- Mimir

- Loki

- Tempo

- HPC

CoreWeave is fascinating because it combines:

Infrastructure Scale

Thousands of servers per cluster.

AI Networking

- InfiniBand

- RoCE

- GPUDirect RDMA

Storage

- High-throughput parallel storage

- Object storage

- Checkpointing

Reliability

When a training run consumes:

10,000 GPUs

×

7 daysa single infrastructure failure can cost millions of dollars.

This creates unique SRE challenges around:

- Cluster reliability

- GPU scheduling

- Capacity management

- Fleet automation

- Telemetry at hyperscale

- AI workload observability

Why CoreWeave is Important

CoreWeave is one of the first companies to prove that a specialist AI cloud provider can compete with traditional hyperscalers.

The company effectively created a new category:

Traditional Cloud

AWS

Azure

GCP

vs

AI Cloud

CoreWeave

Crusoe

Lambda

NscaleThat category is now one of the fastest-growing areas of infrastructure technology and is driving much of the current AI infrastructure build-out worldwide.

CoreWeave’s stock has had one of the most volatile post-IPO journeys in the AI infrastructure sector.

Share Price Since IPO

CoreWeave completed its Nasdaq IPO in March 2025 under the ticker CRWV. The IPO was downsized before launch, raising about $1.5 billion rather than the larger amount initially targeted.

The broad trajectory has been:

| Period | Approximate Story |

|---|---|

| Mar 2025 IPO | Weak initial reception and downsized offering |

| Apr–Jun 2025 | Strong AI enthusiasm drove shares sharply higher |

| Jun 2025 | Reached all-time highs around $187/share |

| H2 2025 | Significant correction as investors focused on debt, losses, and data-centre execution |

| Early 2026 | Recovery driven by AI demand, Anthropic, Meta, OpenAI and enterprise growth |

| Jun 2026 | Trading around $107/share |

Recent trading puts the company at a market capitalization of roughly $56 billion.

The Good News Financially

Revenue Growth Is Extraordinary

CoreWeave is one of the fastest-growing infrastructure companies in the market.

Examples include:

- Revenue more than doubled year-over-year in multiple recent quarters.

- Enterprise adoption is expanding beyond AI labs into financial services and large enterprises.

- Revenue backlog reached approximately $99.4 billion as of Q1 2026.

That backlog is enormous and provides strong visibility into future revenue.

Major Customers

CoreWeave has secured relationships with:

These are arguably the most important AI infrastructure customers on the planet.

Scale Advantage

Reuters recently noted that CoreWeave has:

- More than 1 GW already deployed

- More than 3.5 GW contracted for future deployment

This places it among the largest dedicated AI infrastructure operators globally.

The Risks

Massive Debt Load

This is the biggest concern.

CoreWeave financed much of its growth through:

- Asset-backed debt

- Infrastructure loans

- GPU-backed financing

- Convertible notes

Multiple analysts and investors have pointed to the company’s very large debt burden as its primary financial risk.

The business model requires spending billions before revenue arrives.

Still Losing Money

Despite explosive revenue growth, CoreWeave remains unprofitable on a net-income basis.

Investors are essentially betting that:

Revenue Growth

>

Interest Costs + Depreciation + Expansion Costsover the long term.

Recent earnings showed revenue beating expectations while margins and profitability remained under pressure.

Customer Concentration

Historically, a large portion of revenue has come from a relatively small number of customers.

If:

- OpenAI

- Microsoft

- Meta

- Anthropic

decide to build more capacity themselves, future growth could be affected.

This is one reason investors closely watch customer mix and backlog growth.

Why Investors Still Like It

The bullish thesis is straightforward:

- AI demand continues growing.

- GPU supply remains constrained.

- Training and inference workloads keep increasing.

- CoreWeave owns and operates the infrastructure needed to satisfy that demand.

In that scenario, today’s debt becomes manageable because revenue grows faster than financing costs.

Compared with Nscale

If I compare the two today:

| Area | CoreWeave | Nscale |

|---|---|---|

| Public Company | Yes | Not yet |

| Market Cap | ~$56B | Private |

| Revenue | Multi-billion | Much smaller |

| Operational GPU Capacity | Very large | Limited publicly visible |

| Revenue Backlog | ~$99B | Not publicly disclosed at same level |

| Debt | Very high | Much lower today |

| Execution Risk | Moderate | High |

| Infrastructure Maturity | Established | Emerging |

CoreWeave’s biggest challenge is financial leverage.

Nscale’s biggest challenge is execution.

CoreWeave has already proven it can build and operate AI infrastructure at scale. The question investors are asking is whether it can generate enough cash flow to justify the enormous capital expenditure and debt required to stay ahead in the AI compute race.

Crusoe

Crusoe is arguably the third major AI infrastructure challenger behind CoreWeave and the large hyperscalers, and alongside Nscale and Radiant in the race to build AI factories.

What makes Crusoe unique is that it evolved from an energy company into an AI infrastructure company.

Its progression has been roughly:

Flared Gas Capture

↓

Power Generation

↓

Bitcoin Mining

↓

GPU Infrastructure

↓

AI Cloud

↓

AI FactoriesToday the company describes itself as an “AI Factory Company” rather than a traditional cloud provider.

Current Position

Valuation

Crusoe raised:

- $600M Series D (2024)

- $1.375B Series E (2025)

at a valuation exceeding $10 billion.

There are also industry reports suggesting private-market discussions at significantly higher valuations during 2026, though these are not official company figures.

Funding Strength

Crusoe has now raised approximately:

- $3.8B+ equity funding

- Additional billions in project finance and credit facilities

including a $750M Brookfield-backed credit facility.

Compared with many startups, Crusoe has become exceptionally well capitalized.

The Abilene AI Campus

The company’s flagship project is:

Abilene, Texas

This has become one of the largest AI infrastructure projects in the world.

Public reports describe:

- 1.2 GW campus

- Up to ~400,000 NVIDIA GB200-class GPUs planned

- $15B+ joint venture funding

- Major Oracle/OpenAI involvement

- Multiple operational buildings already online

This campus is one of the key foundations of the Stargate ecosystem.

Relationship With OpenAI, Oracle & Microsoft

Crusoe sits at the center of a fascinating triangle:

OpenAI

│

Oracle

│

Crusoe

│

MicrosoftRecent developments have been mixed:

Positive

Oracle states:

- Abilene remains on schedule

- Two buildings are operational

- Additional Stargate capacity remains under development

Complicated

Several planned expansions have changed tenants or scope.

Reports indicate:

- OpenAI and Oracle stepped back from some expansion plans.

- Microsoft subsequently agreed to lease part of the adjacent capacity.

- Meta has reportedly evaluated some available capacity.

This isn’t necessarily bad news—it may actually demonstrate that demand is broad enough that multiple hyperscalers are competing for capacity.

Revenue Performance

Industry estimates suggest:

| Year | Revenue |

|---|---|

| 2024 | ~$276M |

| 2025 | ~$998M |

| 2026 | Potentially >$2B |

These are not audited public-company figures but are widely cited estimates reflecting the company’s rapid growth trajectory.

If accurate, Crusoe would be among the fastest-growing infrastructure companies globally.

Why Investors Like Crusoe

1. Speed

Crusoe has developed a reputation for building AI infrastructure extremely quickly.

Some investors explicitly cite build speed as a competitive advantage versus traditional data-center developers.

2. Vertical Integration

Unlike many competitors, Crusoe controls:

Power

↓

Generation

↓

Infrastructure

↓

Data Centres

↓

GPU CloudThis resembles Radiant’s strategy and increasingly resembles Nscale’s.

3. AI Factory Focus

The company is moving beyond:

GPU Rentaltoward:

Complete AI Factorieswhich is where the largest contracts are emerging.

Current Challenges

1. Customer Concentration

Much of Crusoe’s growth is tied to:

- OpenAI

- Oracle

- Microsoft

This creates concentration risk.

If one customer changes strategy, large projects can be affected.

2. Capital Intensity

Like CoreWeave, Crusoe requires enormous capital expenditures.

Building:

- Multi-GW campuses

- Power infrastructure

- GPU fleets

requires tens of billions of dollars.

3. Project Volatility

Recent examples include:

- Wyoming project pause

- Changing Stargate scope

- Customer reallocations between OpenAI, Oracle, Microsoft and others

This demonstrates that even the hottest AI infrastructure projects are not immune to execution risk.

How Crusoe Compares

| Category | CoreWeave | Crusoe | Nscale | Radiant |

|---|---|---|---|---|

| Public Company | Yes | No | No | No |

| Valuation | ~$56B market cap | $10B+ private | Private | Private |

| AI Cloud Platform | Mature | Growing rapidly | Emerging | Ori platform |

| Operational AI Infrastructure | Very large | Large | Smaller today | Early |

| AI Factory Focus | Strong | Very strong | Very strong | Very strong |

| Energy Integration | Moderate | Strong | Strong | Exceptional |

| IPO Candidate | Already public | Likely future IPO | Potential IPO | Long-term possibility |

What I Think of Crusoe

Among the “new hyperscalers”:

- CoreWeave is currently the operational leader.

- Crusoe is probably the most advanced private AI infrastructure company.

- Nscale has one of the largest future pipelines.

- Radiant may have the strongest long-term capital structure because of Brookfield.

Crusoe’s biggest strength is that it has already proven it can deliver and operate very large AI campuses while still retaining startup-level speed. Its biggest challenge is moving from a few gigantic flagship projects into a diversified, repeatable AI infrastructure business that is less dependent on any single customer or project.

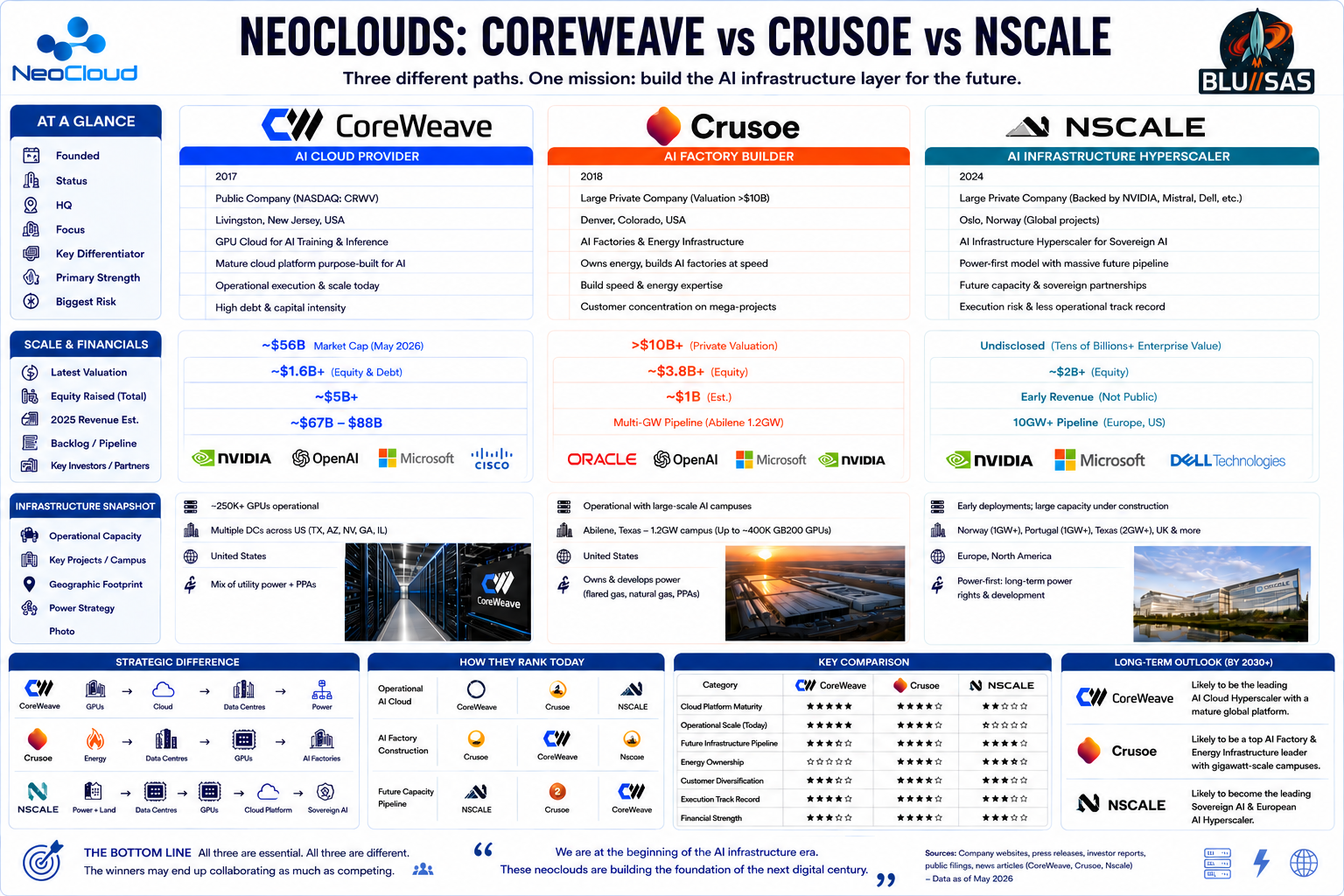

CoreWeave vs Crusoe vs Nscale

These are arguably the three most important “Neoclouds” today.

All three are trying to become the AI-era equivalent of hyperscalers, but they are taking very different paths.

Executive Summary

| Company | CoreWeave | Crusoe | Nscale |

|---|---|---|---|

| Founded | 2017 | 2018 | 2024 |

| Status | Public company | Large private company | Large private company |

| Core Identity | AI cloud provider | AI factory builder | AI infrastructure hyperscaler |

| Geographic Strength | US | US | Europe |

| Operational Maturity | Highest | High | Emerging |

| AI Cloud Platform | Most mature | Growing | Developing |

| Energy Ownership | Limited | Strong | Strong |

| Future Capacity Pipeline | Large | Very Large | Enormous |

| Biggest Risk | Debt | Customer concentration | Execution |

| Biggest Strength | Operational excellence | Infrastructure delivery | Power + future capacity |

CoreWeave is currently winning on execution. Crusoe is winning on AI factory construction. Nscale is winning on future infrastructure ambition.

1. CoreWeave

What CoreWeave Is

CoreWeave is fundamentally an AI-native cloud provider.

Think:

AWS for GPUsexcept purpose-built for:

- AI training

- AI inference

- LLMs

- HPC

Its cloud platform is already mature and heavily used by large AI companies. CoreWeave operates dozens of data centres, hundreds of thousands of GPUs, and has become one of NVIDIA’s most important cloud partners.

Strengths

- Most mature software platform

- Largest operational fleet

- Strong OpenAI, Microsoft, Meta, Anthropic relationships

- Fastest revenue growth

- Proven ability to monetize GPUs

CoreWeave reported more than $5B revenue and a backlog approaching $67B-$88B depending on reporting period.

Weaknesses

- Huge debt load

- Heavy capex requirements

- Customer concentration

- Public market scrutiny

2. Crusoe

What Crusoe Is

Crusoe is best described as:

Energy Company

+

AI Factory Builder

+

GPU CloudIt started by monetizing stranded energy and evolved into building some of the largest AI campuses in the world.

The Abilene campus in Texas has become one of the flagship AI infrastructure projects globally and is tied to Oracle and OpenAI’s broader Stargate ecosystem.

Strengths

- Extremely fast construction capability

- Strong energy expertise

- Large-scale AI factory delivery

- Deep OpenAI/Oracle ecosystem integration

Weaknesses

- Smaller cloud platform than CoreWeave

- Less diversified customer base

- Still heavily tied to a few mega-projects

What Crusoe Wants To Become

Crusoe appears to be evolving toward:

AI Factory Companyrather than simply a GPU cloud.

3. Nscale

What Nscale Is

Nscale is pursuing the most ambitious infrastructure vision.

Their strategy is:

Power

↓

Land

↓

Data Centres

↓

GPUs

↓

Cloud PlatformThey are effectively trying to build a European AI hyperscaler from scratch.

Strengths

- Massive future pipeline

- Strong sovereign AI positioning

- European leadership position

- Large power commitments

- Strong Microsoft/OpenAI/NVIDIA relationships

Weaknesses

- Much of capacity remains future-dated

- Less operational experience

- Less mature cloud platform

- Execution risk

Public reporting has highlighted that several headline projects remain in buildout or planning phases rather than being fully operational today.

The Strategic Difference

CoreWeave

Started with:

GPUsThen added:

Cloud

→ Data Centres

→ PowerCrusoe

Started with:

EnergyThen added:

Data Centres

→ GPUs

→ AI FactoriesNscale

Started with:

Power + InfrastructureThen added:

GPUs

→ Cloud

→ Sovereign AIWhich Company Is Furthest Ahead Today?

Operational AI Cloud

Winner:

🥇 CoreWeave

Reason:

- Largest operational fleet

- Most mature software platform

- Largest customer base

AI Factory Construction

Winner:

🥇 Crusoe

Reason:

- Abilene

- Stargate involvement

- Proven delivery capability

Future Capacity Pipeline

Winner:

🥇 Nscale

Reason:

- Norway

- Portugal

- Texas

- UK projects

- Sovereign AI initiatives

Which Is Closest To Becoming a New Hyperscaler?

Today

CoreWeave

↑

|

Crusoe

|

NscaleBy 2030 (Potential)

CoreWeave

Crusoe

NscaleAll three could be major AI infrastructure providers, but they will likely specialize differently:

| Company | Likely Long-Term Identity |

|---|---|

| CoreWeave | AI Cloud Hyperscaler |

| Crusoe | AI Factory & Energy Infrastructure Leader |

| Nscale | Sovereign AI & European AI Hyperscaler |

From an SRE / Cloud Infrastructure Perspective

If you wanted to work on the most technically mature environment today:

CoreWeave

If you wanted to build some of the world’s largest AI campuses:

Crusoe

If you wanted to help create a new AI hyperscaler from the ground up:

Nscale

That is the clearest distinction between the three companies as of mid-2026.

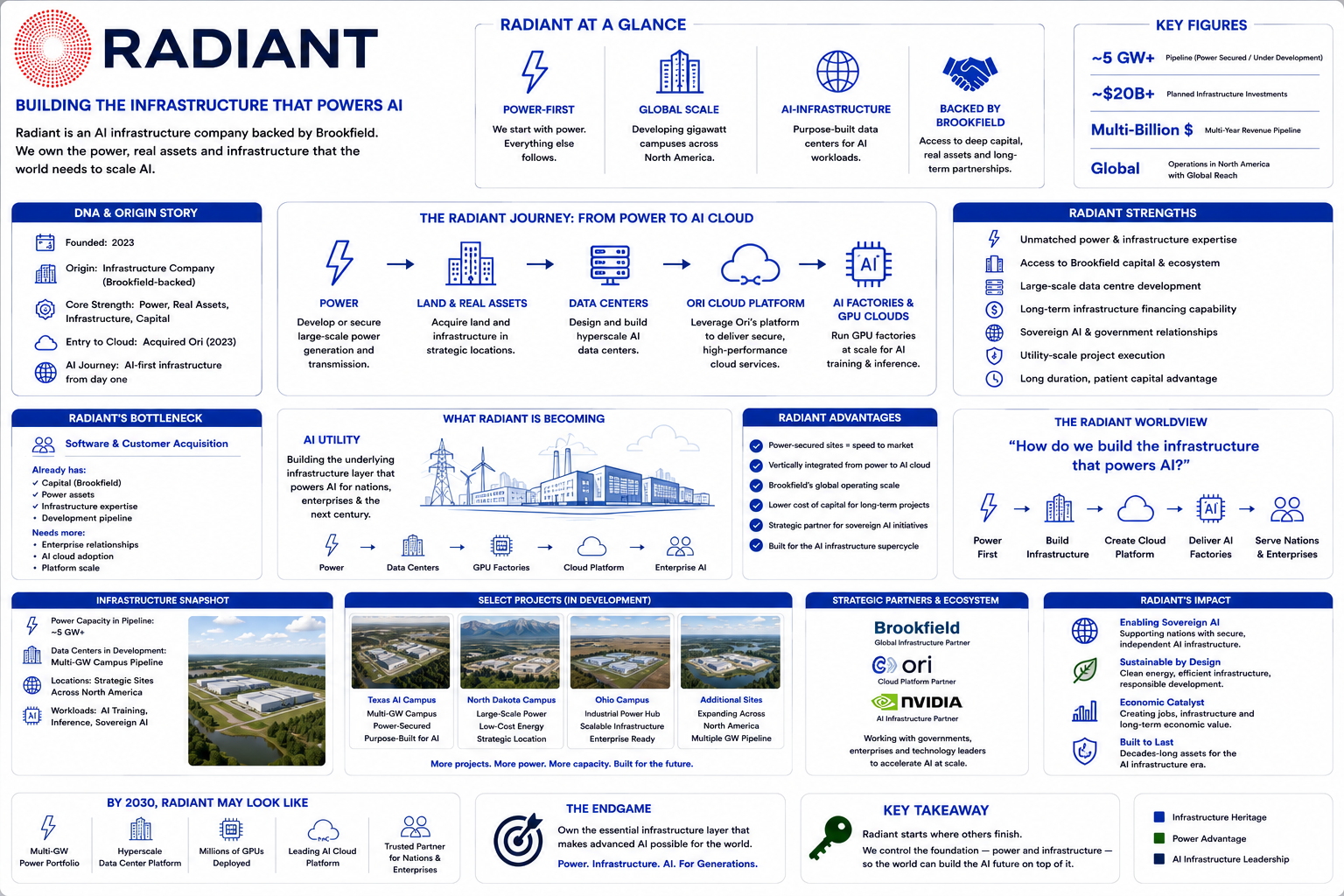

Who is Radiant?

Radiant/Ori is one of the more interesting challengers because they are not trying to copy CoreWeave or Nscale exactly.

Instead, they are attempting to combine:

- Brookfield’s enormous infrastructure and energy assets

- Ori’s AI cloud software platform

- NVIDIA’s AI factory ecosystem

- Sovereign AI demand from governments and large enterprises

into a vertically integrated AI infrastructure company.

What is Ori?

Before the merger, Ori Industries was a UK AI cloud company founded in 2019.

Ori built:

- Distributed GPU cloud infrastructure

- AI model training platforms

- AI deployment services

- Multi-location AI compute services

The company operated AI infrastructure across more than 20 global locations and developed software to orchestrate AI workloads across GPU infrastructure.

Think of Ori as:

What CoreWeave built:

GPU Cloud Platform

What Ori built:

Distributed AI Infrastructure PlatformOri’s technology is arguably the key intellectual property in the merger.

What is Radiant?

Radiant is Brookfield’s AI infrastructure company.

Brookfield is one of the world’s largest infrastructure investors with hundreds of billions under management spanning:

- Power generation

- Transmission

- Renewable energy

- Real estate

- Data centres

- Infrastructure projects

Radiant was created to become Brookfield’s AI compute platform.

Why Brookfield Matters

This is where Radiant becomes potentially disruptive.

Most AI clouds have a structure like:

Raise Venture Capital

↓

Buy GPUs

↓

Rent Datacentre Space

↓

Sell ComputeCoreWeave largely grew this way.

Nscale is evolving toward:

Power

↓

Datacentres

↓

GPUs

↓

Cloud PlatformRadiant starts with:

Brookfield Capital

+

Brookfield Power

+

Brookfield Land

+

Brookfield Datacentres

+

Ori SoftwareThat means they potentially have access to cheaper capital than most AI startups.

Their Stated Strategy

Radiant has publicly described itself as a vertically integrated AI infrastructure platform.

Target customers include:

- Sovereign governments

- Hyperscalers

- Tier-1 telecom operators

- Large enterprises

Rather than simply renting GPUs to startups.

Their focus appears to be:

AI Factories

Large installations of:

- NVIDIA GPUs

- AI networking

- AI storage

- AI orchestration software

built for nations and large corporations.

The NVIDIA Connection

Radiant is built around NVIDIA’s AI factory vision.

Public statements indicate:

- NVIDIA contributed capital to Brookfield’s AI fund.

- NVIDIA will supply GPUs.

- Radiant will deploy NVIDIA DSX AI factories.

This places them squarely in the same ecosystem as:

- CoreWeave

- Crusoe

- Lambda

- Nscale

but with a heavier focus on sovereign infrastructure.

How They Intend to Join the Hyperscaler Club

The strategy appears to be:

Phase 1: Acquire Software

Acquire Ori.

Result:

GPU Cloud Software

AI Orchestration

AI Platform Expertise✓ Completed.

Phase 2: Leverage Brookfield Infrastructure

Use Brookfield’s:

- powered land

- data centres

- energy assets

instead of building everything from scratch.

This is a major advantage versus startups.

Phase 3: Build Sovereign AI Factories

Target:

- governments

- national AI initiatives

- regulated industries

This aligns well with Europe’s push toward sovereign AI and AI factories.

Phase 4: Scale Like a Utility

This is probably the most important difference.

Several executives have stated they want AI infrastructure financed like:

Power Stations

Utilities

Rail Networks

Airportsrather than venture-backed cloud startups.

That could significantly lower financing costs compared with many GPU cloud providers.

How Do They Compare?

| Company | CoreWeave | Nscale | Radiant |

|---|---|---|---|

| Founded | 2017 | 2024 | 2026 |

| Public | Yes | No | No |

| Core Strength | Operating GPU clouds | Building AI campuses | Infrastructure + software |

| Main Backer | Public markets | Investors/NVIDIA | Brookfield |

| Focus | AI cloud | AI hyperscaler | AI utility model |

| Sovereign AI | Moderate | Strong | Very Strong |

| Capital Access | Good | Good | Potentially Exceptional |

| Operational GPU Scale Today | Highest | Lower | Very Early |

What Could Make Radiant Dangerous?

If you look at this as an SRE or infrastructure engineer, the biggest threat to competitors is not technology.

It is cost of capital.

CoreWeave’s biggest weakness is debt.

Nscale’s biggest challenge is execution.

Radiant’s pitch is:

“We already own the power, land, infrastructure financing, and data-centre expertise. We just needed the AI cloud software.”

That is precisely what the Ori acquisition gives them.

If Brookfield genuinely deploys the AI Infrastructure Fund at the scale discussed publicly (up to $10B fund commitments and potentially much larger through co-investment structures), Radiant could become one of the few companies capable of competing with CoreWeave, Nscale, Crusoe, and the hyperscalers in the sovereign AI factory market.

For someone with a background in Kubernetes, OpenStack, HPC, AI infrastructure, observability, Ceph, Slurm, and GPU platforms, Radiant is arguably one of the most interesting companies to watch over the next 2–3 years because they are trying to build the “AI utility company” rather than just another GPU cloud.

Is Radiant Ramping Up Recruitment?

If I were advising Radiant’s leadership after the Brookfield + Ori merger, I would not primarily hire more software developers or more data-centre staff initially.

The biggest challenge is integrating:

Energy Infrastructure

+

Data Centres

+

GPU Factories

+

Cloud Platform

+

Sovereign AIinto a single operating model.

That requires a very specific set of engineers.

Tier 1 — Recruit Immediately

These are the highest-priority hires.

1. Principal AI Infrastructure Architects

Need 5–10 globally.

Background:

- CoreWeave

- Microsoft Azure

- AWS

- Oracle Cloud

- NVIDIA

- Crusoe

- Nscale

Skills:

- AI factories

- Multi-GW campuses

- GPU fabrics

- Infrastructure strategy

These people define the architecture.

Without them everyone builds different solutions.

2. Staff/Principal GPU Platform Engineers

Need 20–50.

Skills:

- Kubernetes

- GPU Operator

- Slurm

- CUDA

- MIG

- NCCL

- DGX/HGX

Responsibilities:

GPU lifecycle

GPU scheduling

GPU utilization

GPU observabilityThese are the people that actually make expensive GPUs productive.

3. Staff Network Engineers

Need 20–40.

The AI industry is becoming:

Network Limited

rather than

GPU LimitedExperience:

- InfiniBand

- RoCE

- EVPN/VXLAN

- Arista

- NVIDIA Spectrum

- Mellanox

Sources:

- Meta

- Microsoft

- NVIDIA

- Oracle OCI

- Azure

4. Site Reliability Engineers

Need 30–60.

Not generic web SREs.

Need:

- Kubernetes

- Linux

- GPU clusters

- Storage

- Automation

Focus:

Reliability

Capacity

Performance

Automation5. Observability Platform Engineers

Need 10–20.

This is where many AI companies are currently weak.

Technology:

- OpenTelemetry

- Prometheus

- Mimir

- Loki

- Tempo

- ClickHouse

- Kafka

Mission:

Observe

Everythingincluding:

- GPUs

- Power

- Cooling

- Storage

- Training jobs

- Networks

This is one of the areas where someone with your background would be valuable.

Tier 2 — Build During Year One

6. OpenStack Engineers

Many sovereign customers still want:

Private Cloudrather than:

Public GPU CloudNeed:

- Nova

- Neutron

- Cinder

- Ironic

Especially for government customers.

7. Storage Engineers

Need 15–30.

Experience:

- Ceph

- Lustre

- BeeGFS

- Weka

- VAST

AI clusters consume storage at enormous scale.

8. Infrastructure Software Engineers

Need 20–50.

Build:

- Fleet management

- Provisioning

- Capacity systems

- Internal developer platforms

Languages:

- Go

- Python

- Rust

9. Platform Security Engineers

Need 10–20.

Focus:

- Supply chain security

- GPU isolation

- Sovereign compliance

- Zero trust

Tier 3 — The Secret Weapon

These are the hires that separate a cloud provider from an AI hyperscaler.

10. HPC Engineers

Need 20–40.

Backgrounds:

- National labs

- Universities

- Supercomputing centres

Skills:

- Slurm

- MPI

- InfiniBand

- Parallel filesystems

These people understand:

10,000 GPU training jobsbetter than most cloud engineers.

11. Power Systems Engineers

This is where Brookfield can dominate.

Need:

- Utility engineers

- Grid engineers

- High-voltage engineers

Most AI companies have very few.

Brookfield already has many.

Radiant should integrate them directly.

12. Cooling Engineers

Future AI factories may be:

100MW+

500MW+

1GW+Cooling becomes strategic.

Need expertise in:

- Liquid cooling

- Direct-to-chip

- Immersion

The Leadership Layer

Radiant’s biggest risk is organizational silos.

Avoid:

Brookfield Team

|

|

Ori TeamInstead build:

AI Infrastructure

|

+-- Energy

+-- Datacentres

+-- GPU Platform

+-- SRE

+-- Observability

+-- SecurityIf I Had £100M Hiring Budget

I’d prioritize:

| Role | Approx Headcount |

|---|---|

| GPU Platform Engineers | 40 |

| SREs | 40 |

| Network Engineers | 30 |

| Infrastructure Software Engineers | 30 |

| Storage Engineers | 20 |

| Observability Engineers | 15 |

| HPC Engineers | 20 |

| Security Engineers | 15 |

| AI Infrastructure Architects | 10 |

| Power/Cooling Specialists | 20 |

Total: ~240 specialist engineers.

The Three Most Valuable Hires

If Radiant could only hire three categories tomorrow:

- Principal GPU Platform Engineers

- Principal AI Networking Engineers

- Principal Observability/SRE Engineers

Those three groups determine whether a 100,000-GPU AI factory operates at:

95% utilizationor

60% utilizationThe difference is potentially hundreds of millions of dollars per year in infrastructure efficiency. For a company trying to become an AI utility, those engineering disciplines are arguably more important than almost any other technical hiring category.

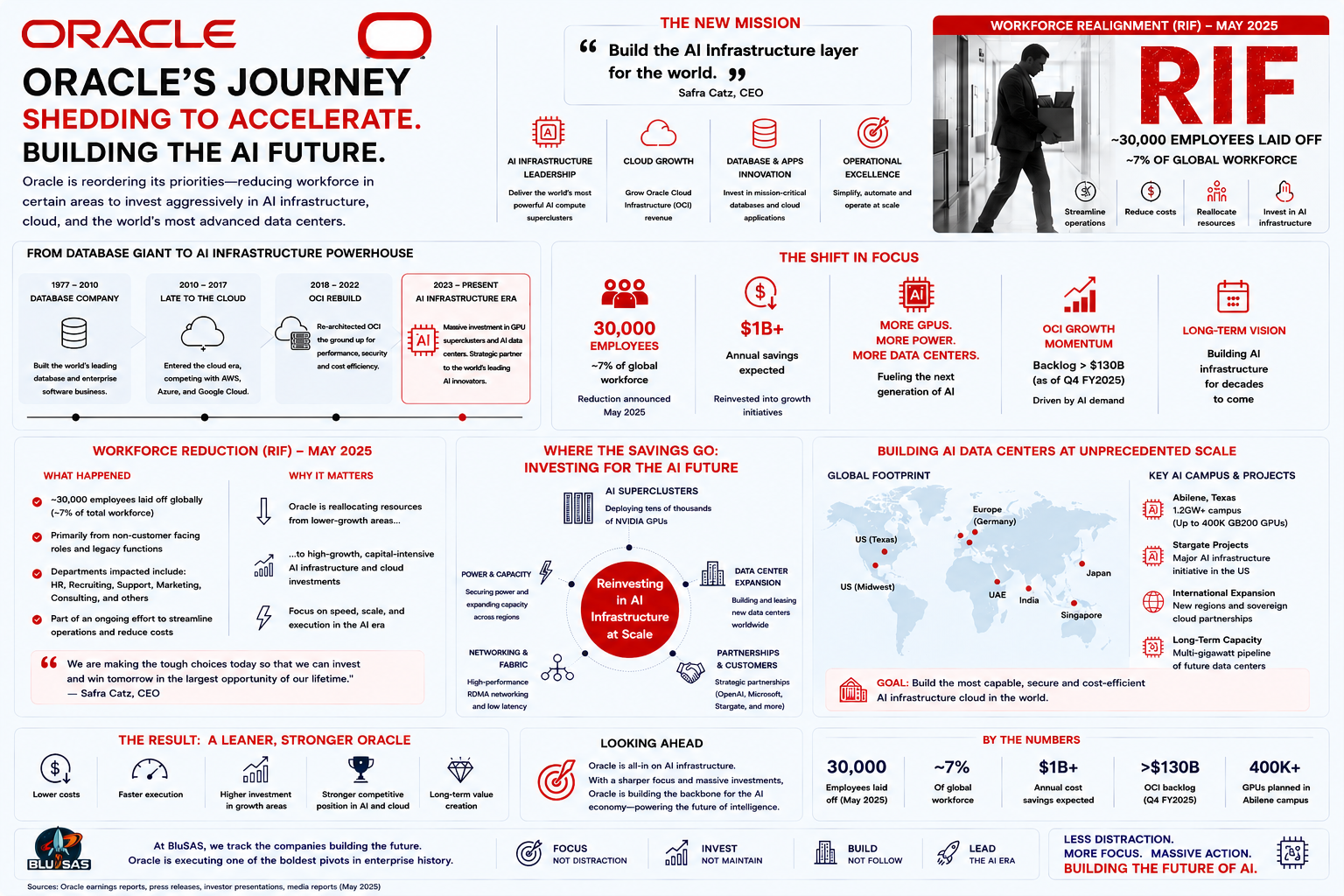

Oracle’s Journey

Phase 1: Database Company (1977-2010)

For decades Oracle was essentially:

Databases

+

Enterprise SoftwareRevenue came from:

- Oracle Database

- Enterprise applications

- Middleware

- Support contracts

Oracle dominated enterprise IT but missed the early public cloud wave.

Phase 2: Late Cloud Entrant (2010-2020)

AWS, Azure and Google Cloud were already well established.

Oracle’s first cloud attempts struggled because they largely tried to:

Move Oracle Products

↓

Into Oracle Cloudrather than building a cloud-native platform.

OCI v1 wasn’t competitive.

Phase 3: OCI Rebuild (2018-2024)

This is where Oracle changed direction.

Under Clay Magouyrk’s leadership, OCI was essentially rebuilt from scratch.

Key design decisions:

Bare Metal First

Unlike AWS:

Physical Server

↓

Hypervisor

↓

VMOCI emphasized:

Physical Server

↓

CustomerThis became attractive for:

- HPC

- AI

- Databases

RDMA Networking

Oracle invested heavily in:

- RoCE

- RDMA

- HPC fabrics

Years before AI made these mainstream.

This is one reason OCI became attractive for GPU clusters.

Autonomous Infrastructure

OCI automated large parts of:

- provisioning

- patching

- operations

allowing Oracle to run cloud regions with fewer people.

Phase 4: AI Pivot (2023-Present)

ChatGPT changed everything.

Oracle suddenly found that:

Their Strengths Were AI Strengths

They already had:

✓ Bare metal

✓ HPC networking

✓ RDMA

✓ Large data centres

✓ Enterprise customers

These are exactly what AI workloads need.

The OpenAI Relationship

This is where Oracle became a serious AI player.

Oracle started providing infrastructure for:

- OpenAI

- Microsoft

- Stargate

through extremely large GPU deployments.

Oracle is now one of the biggest buyers of NVIDIA GPUs in the world.

Oracle’s AI Infrastructure Today

Oracle is building:

GB200 Clusters

Blackwell Clusters

RoCE Fabrics

AI Superclusters

At a scale that rivals many neoclouds.

Some deployments involve:

10,000+

50,000+

100,000+ GPUsdepending on project.

Why Oracle Is Different From CoreWeave

CoreWeave started with:

GPUs

↓

CloudOracle started with:

Cloud

↓

GPUsThis gives Oracle advantages.

Existing Customers

Oracle already has:

- banks

- governments

- telecoms

- healthcare

These customers are now buying AI services.

CoreWeave must acquire those customers.

Oracle already has them.

Existing Revenue

Oracle generates tens of billions annually.

This means they can fund AI expansion from operating cash flow.

CoreWeave relies more heavily on:

- debt

- equity

- project financing

Existing Global Footprint

OCI already operates dozens of regions.

Nscale and Crusoe are still building much of theirs.

Is Oracle Becoming a Hyperscaler?

Oracle already is one.

OCI is generally considered the fourth major hyperscaler after:

- AWS

- Azure

- Oracle

The question is really:

Is Oracle becoming an AI hyperscaler?

The answer is:

Yes.

Is Oracle Becoming a Neocloud?

Not really.

Neoclouds are generally:

AI FirstExamples:

- CoreWeave

- Crusoe

- Nscale

- Radiant

Oracle is:

Cloud First

↓

AI EnhancedA different origin story.

What Oracle Is Morphing Into

I would describe Oracle as:

Traditional Hyperscaler

+

AI Factory Operator

+

GPU Supercluster ProviderIn fact Oracle increasingly resembles:

AWS + CoreWeave

combined.

AWS scale.

CoreWeave-style GPU infrastructure.

Why This Matters for the AI Race

The biggest threat to CoreWeave, Nscale and Crusoe may not be each other.

It may be Oracle.

Because Oracle has:

✓ Existing cloud

✓ Existing customers

✓ Existing revenue

✓ Existing data centres

✓ Existing support organisation

✓ Existing enterprise sales force

✓ Massive GPU procurement

The neoclouds must build these capabilities.

Oracle already has them.

The Next 5 Years

If current trends continue:

| Company | Likely Position 2030 |

|---|---|

| AWS | Largest general cloud |

| Azure | Largest enterprise AI cloud |

| AI + data platform leader | |

| Oracle | AI infrastructure hyperscaler |

| CoreWeave | Largest independent AI cloud |

| Crusoe | AI factory leader |

| Nscale | Sovereign AI hyperscaler |

| Radiant | AI utility platform |

My view is that Oracle is not becoming a neocloud.

Instead, Oracle is doing something arguably more powerful:

It is transforming from a traditional hyperscaler into an AI hyperscaler while retaining all the advantages of an established cloud provider.

That combination of existing scale, enterprise relationships, and AI infrastructure investment is why Oracle has suddenly become one of the most important players in the AI infrastructure market.

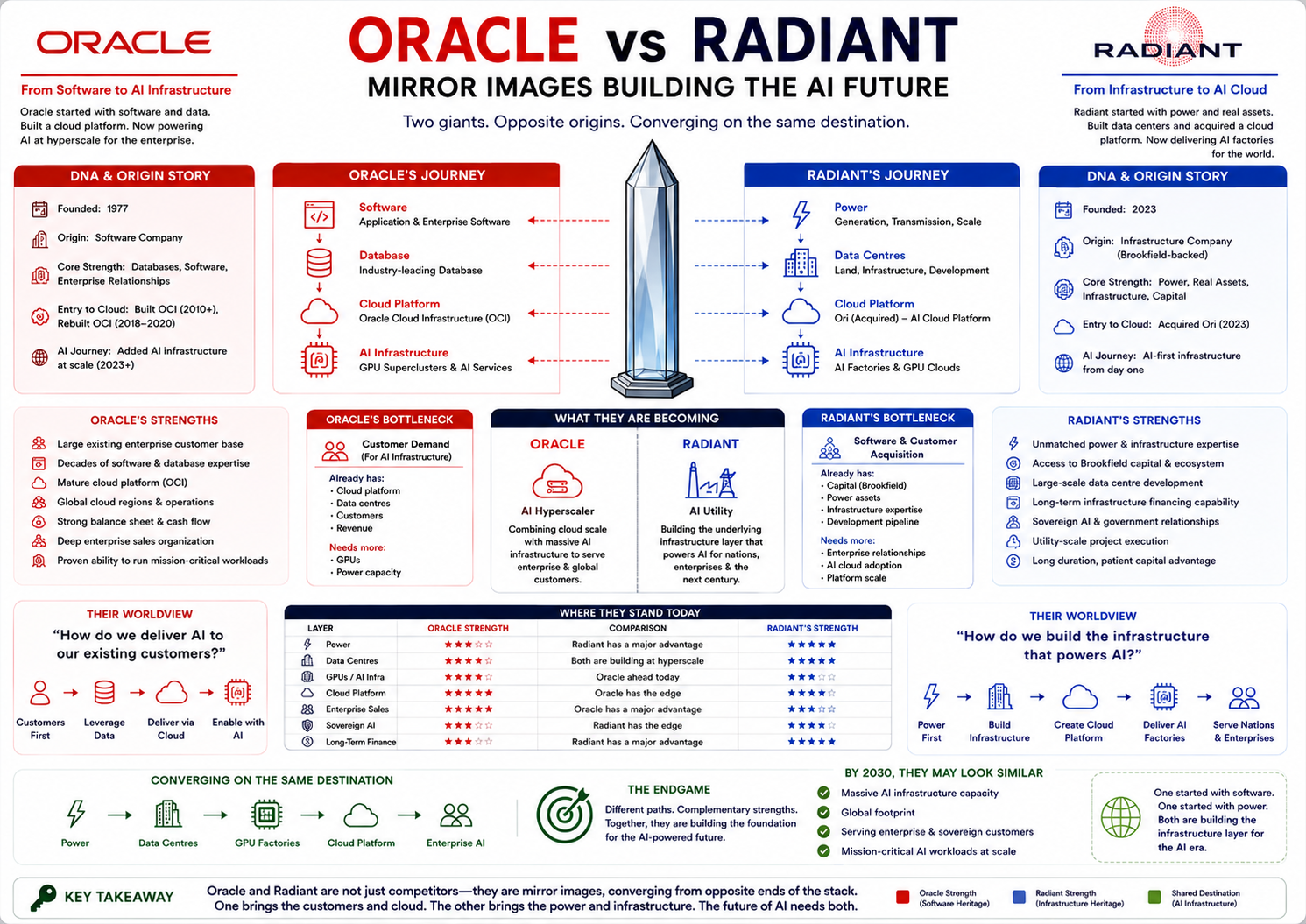

Is Oracle the opposite of Radiant and vice versa?

Not exactly, but they are surprisingly close to being mirror images of each other.

If you look at their origins:

| Oracle | Radiant |

|---|---|

| Started with software | Started with infrastructure |

| Database company | Infrastructure company |

| Built cloud platform | Acquired cloud platform (Ori) |

| Added AI later | Added AI from day one |

| Enterprise customers first | Sovereign AI first |

| Compute-centric | Power-centric |

| Cloud → AI | Infrastructure → AI |

A useful way to think about it is:

Oracle

-------

Software

↓

Database

↓

Cloud

↓

AI Infrastructure

Radiant

--------

Infrastructure

↓

Power

↓

Data Centres

↓

AI InfrastructureSo they are converging on a similar destination from opposite directions.

Oracle’s DNA

Oracle fundamentally thinks like a software company.

Its worldview is:

Application

↓

Database

↓

Cloud Platform

↓

InfrastructureIts biggest assets are:

- Enterprise customers

- Databases

- SaaS products

- Sales organisation

- OCI platform

AI is an extension of those assets.

Oracle asks:

“How do we deliver AI to our existing customers?”

Radiant’s DNA

Radiant fundamentally thinks like an infrastructure company.

Its worldview is:

Power

↓

Land

↓

Data Centre

↓

GPU Factory

↓

AI ServicesIts biggest assets are:

- Brookfield capital

- Brookfield power

- Brookfield real estate

- Brookfield infrastructure expertise

- Ori’s AI platform

Radiant asks:

“How do we build the infrastructure that powers AI?”

The Biggest Difference

Oracle’s bottleneck is usually:

Customer DemandThey already have:

- Data centres

- Customers

- Revenue

They need more GPUs and power.

Radiant’s bottleneck is usually:

Software & Customer AcquisitionThey already have:

- Capital

- Infrastructure expertise

- Energy

They need:

- AI cloud adoption

- Enterprise relationships

- Platform scale

What They Are Trying To Become

Oracle is evolving toward:

AI HyperscalerRadiant is evolving toward:

AI UtilityThose are related but different.

Oracle Vision

Oracle Cloud

+

AI Superclusters

+

Enterprise AIThink:

“AWS/Azure with massive AI capability.”

Radiant Vision

Power

+

Data Centres

+

AI Factories

+

Long-term Infrastructure ContractsThink:

“National Grid meets CoreWeave.”

Why Radiant Could Learn From Oracle

Radiant lacks:

- Enterprise software experience

- Large-scale customer operations

- Decades of cloud platform evolution

Oracle has all of that.

Why Oracle Could Learn From Radiant

Radiant understands:

- Power economics

- Infrastructure financing

- Long-duration capital

- Utility-scale thinking

areas where Oracle historically has less expertise.

If They Met In The Middle

The interesting thing is that both companies are converging toward something like:

Power

↓

Data Centre

↓

GPU Factory

↓

Cloud Platform

↓

Enterprise AIThe difference is where they started.

| Layer | Oracle Strength | Radiant Strength |

|---|---|---|

| Power | Moderate | Exceptional |

| Data Centres | Strong | Exceptional |

| GPUs | Strong | Emerging |

| Cloud Platform | Exceptional | Good (via Ori) |

| Enterprise Sales | Exceptional | Developing |

| Sovereign AI | Moderate | Strong |

| Long-Term Infrastructure Finance | Moderate | Exceptional |

The More Interesting Comparison

I actually think the closest opposite of Radiant is not Oracle.

It’s CoreWeave.

CoreWeave

Started with:

GPUs

↓

Cloud

↓

Data Centres

↓

PowerRadiant

Started with:

Power

↓

Data Centres

↓

Cloud

↓

GPUsThose are almost exact inverses.

Oracle sits somewhere else entirely because it arrived carrying:

Databases

+

Enterprise Software

+

Cloud Platformwhich neither CoreWeave nor Radiant possessed.

So my assessment would be:

- CoreWeave and Radiant are the closest opposites.

- Oracle and Radiant are converging from opposite ends of the technology stack.

- By 2030, Oracle and Radiant may end up looking surprisingly similar externally, even though one began as a software giant and the other as an infrastructure and energy giant.

Reflective Journeys: Oracle vs Radiant

Yes, in many cases Oracle employees affected by AI-related restructuring could be strong candidates for Radiant, but it depends heavily on which part of Oracle they came from.

The interesting thing is that Oracle and Radiant are moving toward the same destination from opposite directions:

Oracle

Database

↓

Cloud

↓

AI Infrastructure

Radiant

Power

↓

Infrastructure

↓

AI InfrastructureThat creates a surprising amount of skill overlap.

Oracle Employees Radiant Should Recruit Aggressively

OCI Engineers

These are probably the highest-value hires.

Experience:

- OCI regions

- Cloud operations

- Bare metal

- Networking

- Cloud automation

Radiant needs people who know how to operate cloud infrastructure at scale.

These engineers bring exactly that.

AI Infrastructure Engineers

Oracle has been building:

- GPU superclusters

- RDMA fabrics

- RoCE networks

- AI training environments

Those skills are directly transferable to:

- Radiant AI factories

- GPU clouds

- Sovereign AI deployments

OCI SREs

Particularly valuable:

- Capacity planning

- Reliability engineering

- Infrastructure automation

- Fleet management

Radiant will need these people immediately as AI factories scale.

Data Centre Engineers

Oracle has been building data centres globally.

Skills:

- Capacity planning

- Facility operations

- Power

- Cooling

- Commissioning

These map extremely well to Radiant’s infrastructure-first strategy.

Network Engineers

Potentially the most valuable category.

Particularly if they have:

- RoCE

- RDMA

- EVPN/VXLAN

- High-performance networking

AI infrastructure is increasingly network-limited rather than GPU-limited.

Observability Engineers

This is a category many AI infrastructure companies underestimate.

Skills:

- OpenTelemetry

- Prometheus

- Grafana

- Logging platforms

- Distributed tracing

Radiant will eventually need to observe:

Power

Cooling

Networks

Storage

GPUs

Training Jobs

Cloud Platformat enormous scale.

Oracle Employees Radiant May Need Less Of

Traditional ERP / Applications Teams

Experience in:

- E-Business Suite

- HR systems

- Legacy applications

is less directly relevant.

Radiant is building infrastructure rather than enterprise applications.

Traditional Database Administration

Still useful, but lower priority.

Radiant’s biggest bottlenecks are more likely:

- GPUs

- Networking

- Data centres

- Cloud platforms

than Oracle Database administration.

Would It Be Good For The Employees?

Potentially yes.

Oracle is becoming:

Large AI HyperscalerRadiant is becoming:

AI Infrastructure Startup

with Brookfield backingSome engineers prefer:

Oracle

- Stability

- Massive scale

- Mature processes

- Existing customer base

Radiant

- Building from scratch

- More influence

- Faster decision making

- Potentially larger individual impact

If I Were Radiant’s CTO

The first Oracle hires I would target would be:

- OCI Principal SREs

- OCI Network Architects

- OCI GPU Platform Engineers

- OCI Capacity Engineers

- OCI Observability Platform Engineers

- OCI Data Centre Build Engineers

These people have already operated infrastructure at scales that Radiant wants to achieve.

Looking at Your Background

Based on the areas you’ve worked deeply in—observability, OpenTelemetry, Prometheus/Mimir/Loki/Tempo, Kubernetes, HPC, storage, automation, cloud platforms, and AI infrastructure—the type of role that would likely be most valuable to a company like Radiant is not a generic SRE.

It would be something closer to:

- Principal Observability Engineer

- AI Infrastructure Observability Architect

- Staff SRE (AI Platforms)

- Platform Engineering Lead

- AI Factory Telemetry Architect

because one of the hardest problems these emerging AI infrastructure companies will face is creating observability across the entire stack:

Power

↓

Data Centre

↓

Network Fabric

↓

GPU Cluster

↓

Kubernetes / Slurm

↓

AI WorkloadsVery few engineers have practical experience spanning that many layers.

One caveat: public reporting has discussed Oracle workforce reductions in various parts of the business, but I have not seen reliable evidence supporting a single confirmed figure of “30,000 layoffs” across Oracle as a whole. When evaluating career moves, it’s better to focus on the strategic trend—Oracle investing heavily in AI infrastructure and cloud—rather than any specific layoff number unless confirmed by Oracle itself.

Where is all the Money?

The short answer is:

The money is real, but most of it is not sitting in a bank account waiting to be spent.

What you’re seeing is a combination of:

- Cash flow

- Debt financing

- Equity financing

- Project finance

- Infrastructure finance

- Customer pre-commitments

- Stock market valuations

The AI infrastructure boom is probably the largest capital deployment into technology infrastructure since the construction of the Internet and mobile networks.

Where Does The Money Actually Come From?

Imagine a company announces:

$20 Billion AI CampusMany people picture:

Bank Account

↓

$20 BillionThat’s almost never what happens.

Instead:

Equity

+

Debt

+

Customer Contracts

+

Infrastructure Loans

+

Future Revenuefund the project.

CoreWeave

CoreWeave is the easiest example.

They need:

- GPUs

- Data centres

- Power

- Networking

worth billions.

They fund this through:

Equity

Investors buy shares.

Debt

Banks lend money.

GPU-backed loans

This is fascinating.

CoreWeave can buy:

100,000 H100sand lenders treat those GPUs almost like collateral.

Similar to:

Mortgage

↔ House

Loan

↔ GPU FleetOracle

Oracle is different.

Oracle generates tens of billions in annual revenue.

Their funding comes primarily from:

Operating Cash Flow

Database Revenue

SaaS Revenue

Support Contracts

OCI RevenueThis is actual cash arriving every quarter.

Oracle can invest from profits.

Corporate Debt

Oracle also issues bonds.

For example:

Oracle Bond

↓

Investors buy it

↓

Oracle receives cashThis is normal corporate finance.

AWS

AWS funding is even simpler.

Amazon generates huge cash flows.

When AWS builds a data centre:

Retail Business

+

AWS Revenue

+

Debt Marketsfund it.

The money is real.

Microsoft

Microsoft is currently spending at extraordinary levels.

Funding comes from:

Windows

Office 365

Azure

GitHub

Copilot

All producing cash.

Microsoft can spend tens of billions annually because they generate enormous free cash flow.

Nscale

Nscale is much more interesting.

Nscale doesn’t have Oracle’s cash flow.

Instead funding comes from:

Equity Investors

Strategic Investors

Infrastructure Finance

Project Finance

Future Customer Contracts

Think:

Power Agreement

+

Land

+

Customer Demand

↓

Banks lend moneyCrusoe

Crusoe is heavily project-finance oriented.

Example:

OpenAI

↓

Needs Capacity

Oracle

↓

Needs Capacity

Crusoe

↓

Build CampusThe campus may be funded by:

- Equity

- Infrastructure loans

- Project financing

- Long-term customer commitments

Similar to how airports and power stations are financed.

Radiant

Radiant may have the strongest financing model.

Why?

Because Brookfield already finances:

- Power stations

- Airports

- Ports

- Railways

- Data centres

worth hundreds of billions.

Brookfield understands:

Build Asset

↓

Generate Revenue

↓

Repay Debtbetter than almost anyone.

Radiant can potentially tap into infrastructure capital that many neoclouds cannot.

Is The Money “Real”?

Yes.

But there are three different meanings.

Real Cash

Example:

Microsoft earns:

$100Customer pays.

Microsoft receives:

$100 cashReal money.

Debt

Example:

Bank lends:

$10 Billionto build AI infrastructure.

Also real money.

But must be repaid.

Market Valuation

This is where people get confused.

Example:

CoreWeave market cap:

$56 BillionThat does NOT mean:

$56 Billion cashexists.

It means:

Share Price × Shares Outstandingequals $56B.

Much of that value exists “on paper.”

The Hidden Fuel: Pension Funds

Most people don’t realize who ultimately finances much of this.

The money often comes from:

- Pension funds

- Sovereign wealth funds

- Insurance companies

- Infrastructure funds

For example:

Teacher Pension

↓

Infrastructure Fund

↓

Brookfield

↓

AI Data CentreThe chain can be surprisingly long.

Why Everyone Is Comfortable Lending

The reason banks are willing to lend is simple:

They believe AI demand will continue growing.

Their assumption is:

GPU Demand

>

Debt CostIf true:

- Loans get repaid.

- Investors make money.

- Infrastructure grows.

If false:

- Some companies will fail.

- Some campuses will be underutilized.

- Some lenders will take losses.

The Biggest Risk

The entire AI infrastructure sector is making a giant bet:

Future AI DemandIf AI demand keeps growing:

- Oracle wins.

- Microsoft wins.

- CoreWeave wins.

- Crusoe wins.

- Nscale wins.

- Radiant wins.

If demand slows dramatically:

The most leveraged companies suffer first.

That is why investors currently view:

| Company | Financial Risk |

|---|---|

| Microsoft | Low |

| Oracle | Low |

| AWS | Low |

| Low | |

| Radiant/Brookfield | Moderate |

| Crusoe | Moderate |

| Nscale | Moderate-High |

| CoreWeave | High |

The hyperscalers are largely spending from enormous existing cash flows. The neoclouds are spending mostly against future growth, future contracts, and infrastructure financing. The money is real, but much more of the neocloud funding stack depends on future demand continuing to justify today’s investments.

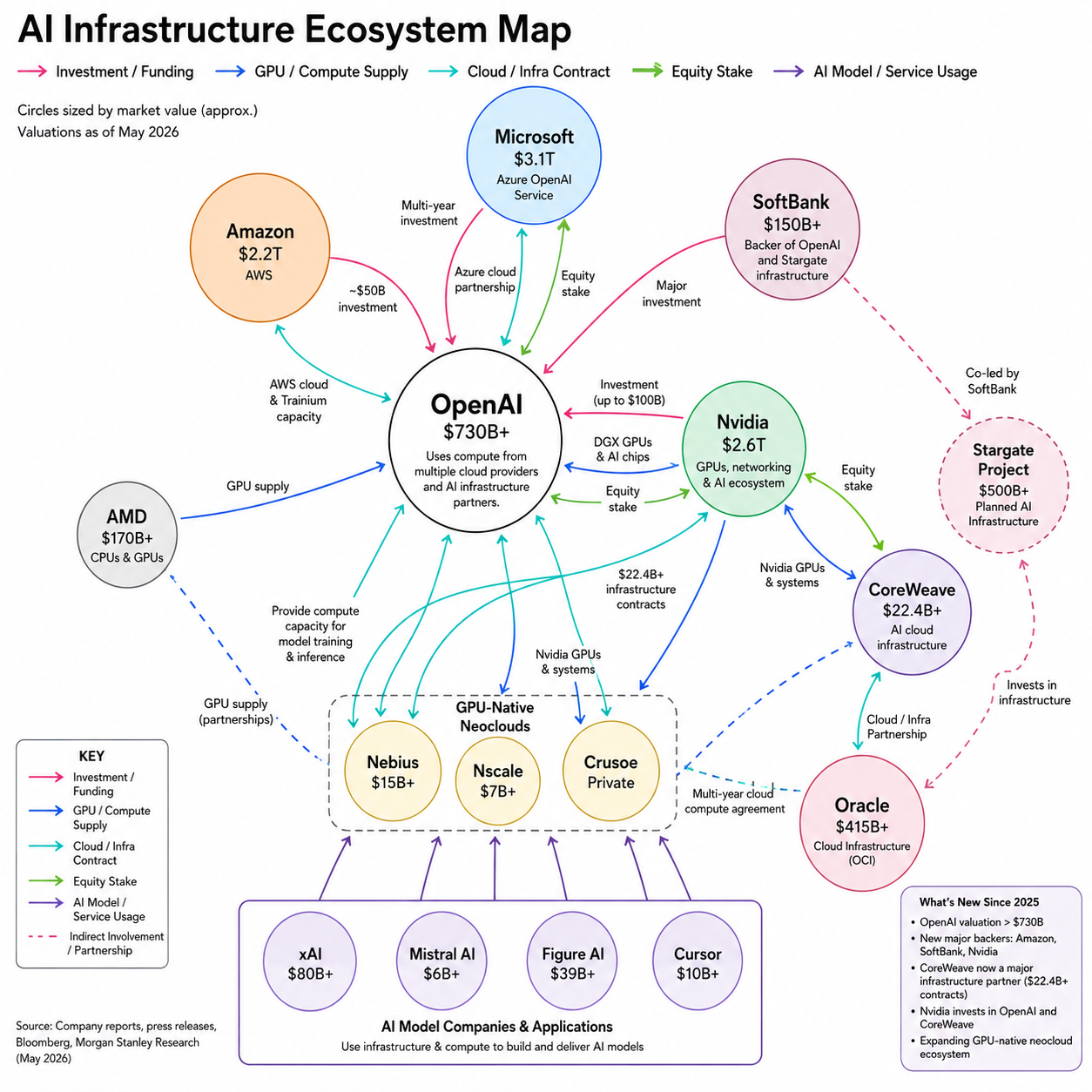

The 2026 AI Funding Diagram

Key changes since the Bloomberg/Morgan Stanley “AI Money Machine” chart from late 2025

OpenAI

- Valuation increased from roughly $500B to over $730B–850B after its record funding rounds in 2026.

- New major funding sources:

- Amazon

- SoftBank

- Nvidia

- OpenAI is now much less dependent on Microsoft than the original chart suggests.

Amazon (missing from the original)

Amazon is arguably the biggest omission now:

- Invested approximately $50B in OpenAI.

- Expanded AWS compute commitments.

- OpenAI agreed to use AWS infrastructure and Trainium capacity.

SoftBank (missing from the original)

- Became one of OpenAI’s largest financial backers.

- Major participant in Stargate-style infrastructure funding.

CoreWeave

- OpenAI relationship expanded to about $22.4B in AI infrastructure contracts.

- Now one of OpenAI’s largest compute suppliers.

- Public company rather than private neocloud startup.

Nvidia

- Still sits at the center.

- Added direct investment into OpenAI.

- Continues investing in CoreWeave while simultaneously selling GPUs to it and buying capacity from it.

Nscale and Nebius

- The original chart correctly anticipated their importance.

- They now fit into a larger category of “GPU-native neoclouds” alongside CoreWeave.

- Their role is increasingly as infrastructure providers for AI model companies rather than model developers themselves.

If Bloomberg redrew it today

The centre would probably look like:

Microsoft

|

|

Amazon ----\

\

SoftBank ----> OpenAI <---- Nvidia

/ | \

/ | \

/ | \

Oracle CoreWeave AMD

| |

| |

GPU Clouds (Nebius, Nscale)

|

Mistral / xAI / Figure / CursorThe biggest differences

| 2025 Chart | 2026 Reality |

|---|---|

| Microsoft dominates OpenAI funding | Amazon + SoftBank now rival Microsoft |

| CoreWeave is peripheral | CoreWeave is a central infrastructure supplier |

| Amazon absent | Amazon is one of the largest players |

| SoftBank absent | SoftBank is one of the largest financiers |

| OpenAI ≈ $500B | OpenAI > $730B valuation |

| Nscale/Nebius niche | Nscale/Nebius increasingly recognized as AI infrastructure providers |

For your interests in AI infrastructure, neoclouds, and hyperscalers, a more useful 2026 version would actually be an “AI Infrastructure Ecosystem Map” showing:

- Nvidia

- AMD

- OpenAI

- Microsoft

- Amazon

- Oracle

- SoftBank

- CoreWeave

- Nebius

- Nscale

- Crusoe

- xAI

- Mistral

- Figure AI

- Stargate

with arrows for:

- Capital investment

- GPU purchases

- Cloud contracts

- Equity stakes

- AI model consumption

That would better reflect where the industry sits today than the original Bloomberg graphic.